The Progressive Case for a Flat Tax

Why flat isn't flat and progressive isn't progressive

Since the creation of the Income Tax in 1861, it has consistently had a progressive structure. The general details of which have been as follows… Income is separated by brackets, with the first bracket of income being fully exempt from taxation and all following brackets of income being taxed at incrementally rising rates. A system that is easy enough to wrap your head around (although a surprising number of Americans don’t). Over this long history, Progressives have generally been the most ardent supporters of this bracketed structure, doing so on the basis that it places a greater tax burden on the rich and a lower one on the working and middle classes.

It was not until the dawn of Milton Friedman's seminal work "Capitalism and Freedom" that an alternative idea of applying one uniform tax rate to all income came into the political vogue, garnering the support of many libertarians and conservatives alike. The key behind its appeal? The promise of a tax system that is far more efficient, fair, and simple. Yet, despite being around since the early 1960s, the idea of a Flat tax has thus far not been implemented (at the federal level), largely because it has failed to secure broad enough appeal across the ideological spectrum. While it has been of frequent mention in Republican primaries, largely thanks to Steve Forbes's campaigns in 1996 and 2000, it has never made it into the policy agenda of any successful Democratic candidate for federal office.

This is largely because the assumption has been that a Flat Tax is necessarily going to be less progressive than a Progressive Income Tax. Many on the political Right have found this to be tolerable, insisting that they will cut spending enough so that even the poor receive a tax cut. Others have produced so-called “Flat” tax proposals that include a large standard deduction, which I would argue, would still be a Progressive Income Tax, just with only two brackets. But Progressives, understandably, have been far less willing to embrace tax reform that they believe will negatively impact low earners and positively impact high earners.

The only issue is, that this shared view - that Flat taxes are by their nature less progressive - is actually incorrect. It relies on a fundamentally incomplete view of the distributional effects of government policy. Taxation does not exist in a vacuum, it is merely the way the government receives revenue. Equally as important is how the government spends it. In order to determine the total distributive impact of government policy, we must look at both taxes and transfers simultaneously. As I will show, when we make use of this more holistic approach, there is indeed a strong case for a Flat tax, not simply on the grounds of efficiency and equity but also progressivity.

I. THE BASICS

The Progressive Income Tax is not nearly as "Progressive" as its name implies.

To illustrate why let's take a look at a simple progressive tax system. It has three brackets, 10% on the first 50,000 dollars, 20% on the next 100,000, and 30% on the rest. Under this system, a family that makes the median household income of $67,521 would be liable to pay $8,504 (12.6% of their income); meanwhile, a family making an income at the threshold of the top 1%, $540,837, would be liable to pay $142,251 (26.3% of their income).

This would seem to demonstrate the case for the Progressive Income tax, i.e., that it takes more as a percentage of income from those most able to pay. But the issue with such a simplistic analysis is that it doesn't consider the opportunity cost. By having reduced rates on the first two brackets of income, the government misses out on a lot of revenue it would have otherwise received. This revenue could have been put towards spending, which also had a progressive effect on income distribution. A fair comparison must account for this.

To make the revenue trade-off clearer, I find it helpful to reconceptualize our view of the Progressive bracket structure. Rather than viewing it as an income tax that has reduced rates for lower-income brackets, we can also look at it as a flat tax with an annual tiered wage subsidy. While, intuitively, taxing certain things less than other things seems different than a subsidy, in economic terms, there is little distinction. A Flat 30% Tax on all income that includes a 29% after-tax subsidy for the first $50,000, and a 14% after-tax subsidy for the next $100,000 would be equivalent to the progressive bracket system outlined earlier.

II. PROGRESSIVITY

Viewing lower rates on lower-income brackets as a form of spending reveals a glaring truth about them, they actually benefit the rich more than the poor. This is because progressivity is defined very differently for spending than it is for taxation.

Progressive taxation is defined as a percentage of income, while spending progressivity is defined in raw terms. A tax cut that gives poor people an average benefit of $1000 and rich people an average benefit of $5000 dollars can still be considered "progressive," so long as the $1000 for the poor represents a larger percentage of their income than the $5000 for the rich. Simultaneously, a spending proposal that had those exact distributional effects would be considered highly regressive because it gave the rich a greater total amount than the poor.

When considered as spending, reduced rates on lower brackets/annual wage subsidies become very clearly regressive. To see precisely how, let's look at how the benefits are distributed among a few hypothetical individuals with very different socioeconomic statuses.

Person A makes $0

Person B makes $50,000

and

Person C makes $1,000,000

Under the Progressive Tax system outlined earlier, Person A receives no benefit whatsoever from the wage subsidy. Obviously, the wage subsidy only goes to those who have wages, thereby excluding the most in need, including the unemployed, students, the elderly, and the disabled, from receiving anything.

Person B receives some benefits, gaining a total of $10,000 from the reduced tax rate, equivalent to 20% of their income. Person C, on the other hand, clearly the least needy of the group, receives the largest benefit by far, at $20,000. This is because Person C earns enough to max out the subsidy/reduced rate in both the $0-$50,000 bracket and the $50,000-$150,000 bracket.

From this example, we can see how backward the Progressive Income tax is. Individuals with no income receive no benefit from the wage subsidy, individuals with low incomes only get meager benefits, and high-income individuals are all awarded the maximum benefit. Progressives would criticize any program with a similar distributional effect for being a regressive giveaway to the rich. It is only because the Progressive bracket structure is viewed as a tax cut rather than spending that its regressive effects are made opaque.

III. THE COSTS

For its minor benefits in terms of distribution, the Progressive Income tax incurs costs in terms of efficiency and fairness. While a flat tax could be easily gathered with no need for taxing filings via an automatically withheld payroll tax (which is already done to fund programs like social security and unemployment insurance), an income tax requires far more work on behalf of the tax authorities and (in most cases) individuals. Countries like Sweden and the UK have made the income tax more workable with advanced tax withholding and pre-filled tax forms. But even with these more advanced variants, progressive income taxes still often require individuals to send an extra check in at the end of the year.

In addition, Progressive Income taxes punish people with irregular incomes by forcing them to pay higher effective tax rates. Let's take a simple example of two people who make $500,000 over five years. Charlotte is a self-employed entrepreneur and makes all her wages in year five, living a meager existence off of savings and debt in the first four years. Meanwhile, Elise, an accountant with a nice stable upper-middle-class job, receives her income evenly divided over each of the five years.

In this hypothetical, poor Charlotte is required to pay $130,000 (26%), while Elise only has to pay $75,000 (15%) even though they both have made the same income! There is no good reason why they should be paying such wildly different rates. In just five years, this unfairness cost Charlotte $55,000 dollars; if we extend the timeline from 5 years to total lifetime income, these variations would be even larger.

< FOOTNOTE > If Charlotte was aware of this disparity, one strategy she could use would be to create a form an LLC and then provide herself with a salary from that business, incurring the debt needed to provide for herself in the first 5 years not personally, but rather to the business. But this strategy would still retain some of the inequity and not all people with irregular incomes will be informed enough or capable of employing such tax saving strategies.

And it's not just Charlotte who loses from this bias; many people have irregular and/or incomes that are concentrated in fewer tax years. A great example is students who sacrifice years of labor force participation for higher wages in the future. The result, at the systemic level of the Progressive Income tax, is a very substantial redistribution from those who have irregular incomes and incomes concentrated in fewer than average years to those who have stable incomes spread over many years. Under a flat tax, how income is spread over tax years is completely irrelevant because all people, regardless of the year of income, pay the exact same rate. No distortions and no inequities.

IV. AN ALTERNATIVE

By eliminating the tiered annual wage subsidy in the income tax and thereby switching to a Flat tax, the government would receive an abundance of extra revenue that could be used in far better ways.

The government could provide a form of Universal Healthcare or a Universal Basic Income. It must be remembered that all that is required to beat wage subsidies in terms of progressivity is a benefit that leaves the poor with more than nothing and the working class with benefits more than half that of the well-off.

A UBI/Universal Cash rebate would probably be the most natural fit for the use of the additional revenue since it would directly show Americans that, even though they may be paying a higher tax rate, at the end of the day, they are left with more cash than they were before. In addition, this tax rebate could be branded as a fully refundable tax credit, so we technically claim that "we aren't raising taxes; we are just cutting them more for lower earners."

Political benefits aside, a Universal Basic Income like direct cash transfer to all Americans would also be relatively easy to administer, highly equitable, since it would be provided to all regardless of income distribution over time, and most importantly, very effective at reducing poverty and inequality. Other alternatives, like the Negative Income Tax, would lack these benefits, creating new implicit taxes via means testing that reduce the supply of labor (even more than explicit taxes do), and exacting a higher administrative burden.

V. CRITIQUES

Despite the (I think) compelling case, I have made for switching to a flat tax; there are still some arguments that can be made to the contrary. In this section, I will briefly go over some of the counter-arguments I anticipate. If you feel fully satisfied with my argument or are prone to falling asleep when encountering clunky academic vernacular, feel free to skip this section. Alternatively, in the case that, after finishing this essay, you still find yourself unconvinced, I invite you to leave a comment explaining your thought process.

Your Flat tax only is more progressive because it generates more revenue, revenue which could be raised by increasing progressive taxes.

Baked into my argument for a flat tax is the idea that rather than applying a low flat tax on everyone (as advocates on the Right have typically proposed), we would apply a rate equal to or somewhat near the top tax rate. Some may view this as a red herring, arguing that if we hold revenue constant, Progressive Income taxes are more progressive than Flat taxes. This statement is true! But I don’t see any good reason why we should do this.

We only care about tax rates in the first place because we believe they influence behavior. Our fundamental underlying assumption is that if you tax somebody when they do something, they will usually do less of it.

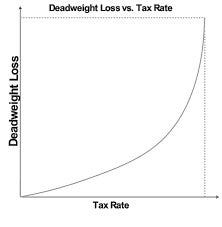

But clearly, people are far more responsive to taxation in some instances than others. For this reason, my argument relies not on holding revenue constant, which could imply wildly different effects on the supply of labor but rather a total impact on deadweight loss. Put in simpler terms, my comparison centers on contrasting the redistribute potential of Progressive Income Taxes and Flat Taxes when we design both to have exactly equivalent effects on economic efficiency.

To determine at which level a Flat Tax and a Progressive Income Tax have the same effect, I use a very basic model of labor tax elasticity (how much people respond to tax rates by working less). My model assumes that labor elasticity starts out extremely low and grows as tax rates climb. I believe a 30 percentage point increase in taxation, from 0% to 30% will have a far smaller impact on people’s decision to pursue earning more than an increase from 50% to 80%. In other words, each percentage point of taxation has more of a negative impact than the last.

If we believe negative effects are exponentially increasing with tax rates, for the same revenue, a Progressive Income tax decreases labor supply more than a Flat Tax. This is because the labor supply savings the Progressive tax yields from having lower taxes for the lower income brackets are more than offset by, the higher tax rates it must enforce on higher brackets. These effects do not balance out because, as mentioned earlier, the impact of each point of taxation is more than the last.

Given that the impact of the Flat tax is less for any given level of revenue, if we adjust it to have a rate that matches the total impact on labor supply, it will raise substantially more revenue than the Progressive Income Tax.

Ample evidence from higher tax nations indicates that the function that defines the relationship between total labor supplied and tax rate is exponential. Essentially, the rate at which taxation starts to have a negative impact is pretty high and increases quickly from there. Taxation in the 40-50% range seems to be a relatively safe zone. These findings strengthen the case for a Flat Tax because the greater the exponentially, the greater ability of a Flat Tax, when using its extra revenue for transfers, to beat the Progressive Income tax in terms of progressivity while holding the impact on Labor Supply constant.

The rich are less responsive to taxation. A Flat tax would not take advantage of this.

Some may argue that people are less responsive to tax rates at higher incomes than they are at lower incomes. It is possible that a person will be more disincentivized by a 30% tax rate on their $50,000 than on their income over $150,000. If this was the case, then it may indeed make sense to tax more lightly income in lower brackets.

Though, I think it’s far more likely, if anything, that the opposite is the case. To the extent that people respond to tax rates by working less, there is reason to think this responsiveness would increase, not decrease, with income. As is widely accepted, there is a diminishing marginal utility of money. Every dollar of income has less of an effect on a person’s well-being than the dollar preceding it. Obviously, a hundred dollars to a homeless man is worth a lot more than it is to a billionaire. Given that this is the case, there is already a naturally diminishing incentive to labor more/harder, a progressive utility tax of sorts. Having an additional progressive tax on top of this effect would only exacerbate the diminishing incentive to labor.

Another way to view this is that for every dollar of additional earned income, there is a slowly rising hidden tax rate. This means that even flat taxation on higher incomes will push their total tax rate (explicit + the hidden utility tax) higher than lower incomes, thus generating more of a negative impact on the quantity of labor supplied. The natural response to this assumption would be to, at a certain point, make tax increases regressive across the board so as to minimize the effect of taxation on labor supply. Though I think this phenomenon is not significant enough, nor worth the distributional effects, to justify such an approach.

A Flat tax is better than what we currently have, but it's not as good as a Fair tax.

Fair Taxes are a set of proposals that seek to replace all or nearly all federal taxes with a national sales tax or value-added tax. The idea is often mentioned in the same breath as the Flat Tax, usually followed by a low-intensity back and forth on which would tax reform would be ideal.

Unlike more right-leaning tax reform proponents, I tend not to think of this as a VAT and Flat tax as an either-or choice. To finance a strong welfare state and all the other policies worthy of government investment will require a significant amount of revenue. Under a reworked tax system, it makes sense to have both a broad-based tax on consumption, a tax on labor, and a tax on the supernormal returns of capital.

This is due to administrative, compliance, political, progressivity, and even efficiency reasons. These taxes should be employed only after Pigouvian taxes, Land taxes, and usage fees have been fully applied when appropriate.

While the especially keen tax experts reading this will probably know that the long-run tax base of a payroll tax + tax on supernormal returns is the same as a value-added tax, what this analysis misses is the short-run incidence. A VAT taxes all preexisting wealth, while payroll taxes and taxes on supernormal returns do not. There also may be a case for other taxes in excess of these; a large promising literature exists on the Inheritance Tax, which may be able to target generational wealth inequality without requiring double taxing all savings regardless of use. These topics deserve a blog post of their own, so I will elucidate more on them when I have the opportunity in the future.

In conclusion, when we start looking at both taxes and transfers rather than just taxes, we find there is indeed a strong progressive case for a Flat tax. With the primary qualm of Democrats addressed, there may just be the grounds for forging consensus needed to transition to one. That is if Republican politicians are willing to tolerate a tax reform that would actually benefit the poor and not the rich.