Tax Reform in the Lone Star State

Psssst... soaking the poor isn't the solution

Over the past few years, tax reform has been all the talk in Texas politics. Since 2019 Republicans have been attempting to replace property taxes with a massively increased sales tax. A move that, according to the Texas Comptrollers’ office, would require sales taxes to be raised to 25%. Have no doubts; this is an absolutely terrible idea. It would massively increase tax avoidance, push many Texans into poverty, and actually, contrary to their claims, reduce growth.

This plan is bad, but it does bring up the valid question, what would genuinely positive tax reform look like in Texas? Given that I have already created a proposal for improving local and federal tax policy, it's about time I finally tackle the surprisingly bad tax code of Texas.

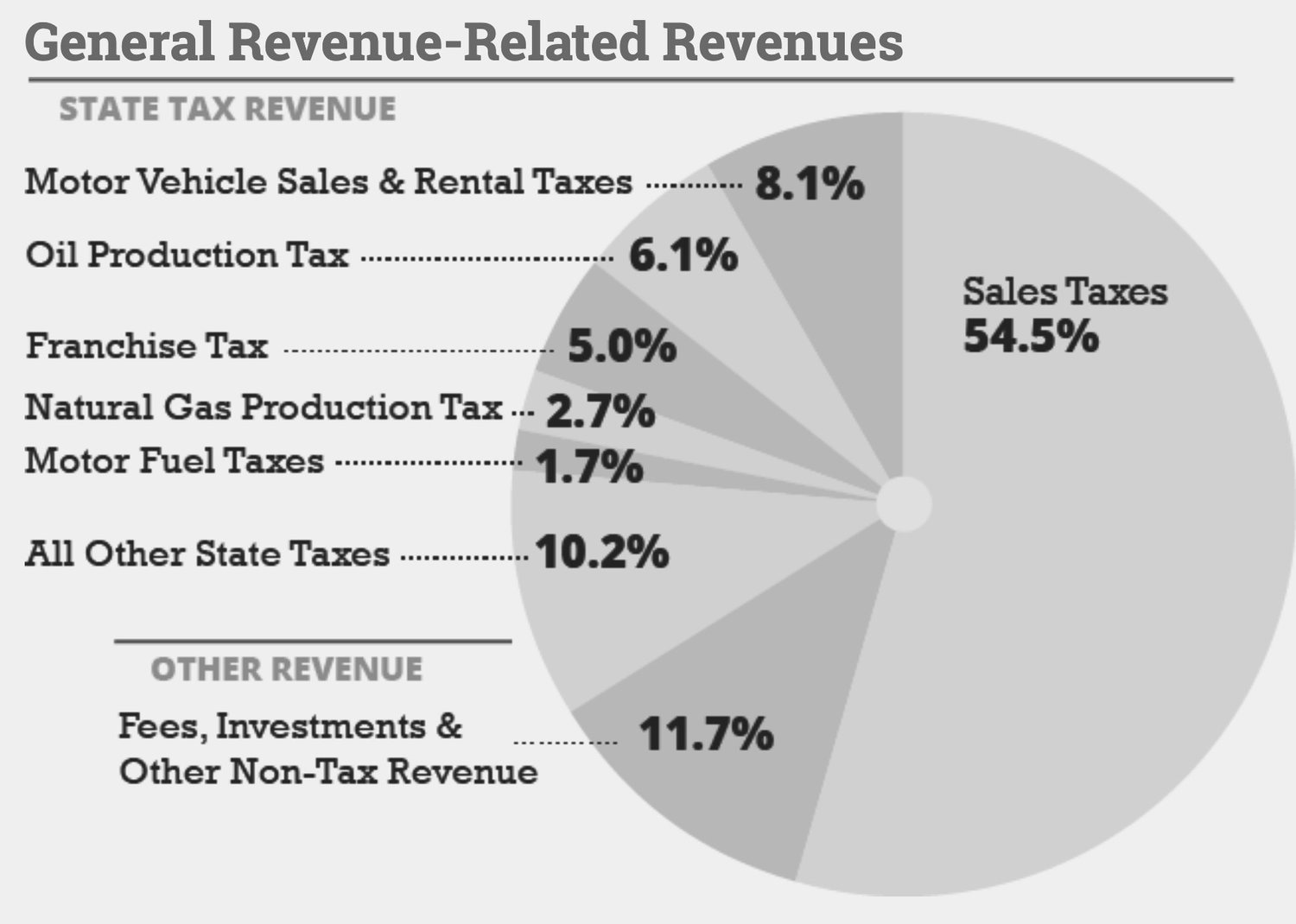

As you can see from the above chart, the majority of state revenue in Texas comes from the retail sales tax, with the rest of the revenue coming from a bunch of smaller taxes, including a couple of gross receipts taxes and a few severance/extraction taxes. To differing degrees, many of these taxes are problematic. In the following section, I will break down these areas of problematicness into three categories, inefficiency, insufficiency, and regressivity.

1. The Problems

A. Inefficiency

While often touted by Republican Politicians as being highly efficient, the retail sales tax, especially of the structure being used in Texas, is actually a bit of a disaster. Under the current law, the sales tax only hits some goods and misses many services. The effect of this is that the goods/services that don’t get hit by the tax appear comparatively affordable, and the public is deprived of billions in revenue every year. In isolating the cause of these issues, I have identified a couple of primary culprits…

EXEMPTIONS - One reason so many things go tax-free is the poor language of the law. Nonsensically, the state of Texas has chosen to only apply taxes to specifically defined services rather than all services, as is done in states like Hawaii and New Mexico. This means that every service not specifically mentioned in the tax code is completely free from tax liability! In addition, generous exemptions have been granted to a whole range of commodities for seemingly no justifiable reason, including groceries, utilities, gas, and newspapers, among others.

SOURCING RULES - Another cause of the problem is Texas's complicated and inconsistent sourcing rules. Sourcing rules are the legal rules that determine, in cases where a transaction happens between parties in separate jurisdictions, which jurisdiction gets to charge the sales tax. Since, in the contemporary United States, buyers and sellers are often in different locations, using the internet, mail-order, or telecommunications to facilitate exchange, sourcing rules are incredibly important for sales taxes to work properly.

Most states/local governments use either destination or origin sourcing rules, whereby taxes are applied at the seller's location or the buyer's. But Texas uses a form of mixed sourcing rules, where sometimes it applies origin rules and, other times, destination. As any Tax Lawyer in Texas knows well, the law as it stands is highly contradictory and difficult to comply with. Accordingly, many transactions go tax-free because of these poorly conceived rules, leading the state to miss out on a substantial sum of revenues.

ENFORCEMENT - Finally, the last big contributor to the issue is the inherent difficulty of enforcement that comes with vendor-based taxes. Sales taxes require vendors themselves to gather the tax and provide it to the state. To fully enforce the tax, the state would have to know every retail transaction that occurs in the entire state, including those that happen with one of the transacting parties being outside the state. This is, of course, simply not possible, and thus a lot of vendors get away without charging the tax.

But unfortunately, gaps in the base are but one issue with the retail sales tax. Just as often as it misses transactions that it should be taxing, it ends up hitting transactions it should most definitely not be taxing. Presently, the sales tax often hits business-to-business transactions. A study by the Brooking Institute found that roughly 40% of sales taxes, on average, are paid not by consumers but by businesses. A different study, this one by the Council on State Taxation, found that Texas's sales tax is actually worse than average in this regard, getting a whopping 52% of its revenue by taxing business inputs.

For those who don't know, a *RETAIL* sales tax is supposed to only hit the final sale of a good to consumers. It is certainly *NOT* supposed to hit the business transactions within the supply chain of creating a product or service. The effect of taxing inter-business transfers as Texas is currently is disastrous. Smaller businesses are put at a systemic disadvantage when compared to their larger competitors, who can do everything in-house. Furthermore, investment is reduced because the tax artificially jacks up the cost of capital.

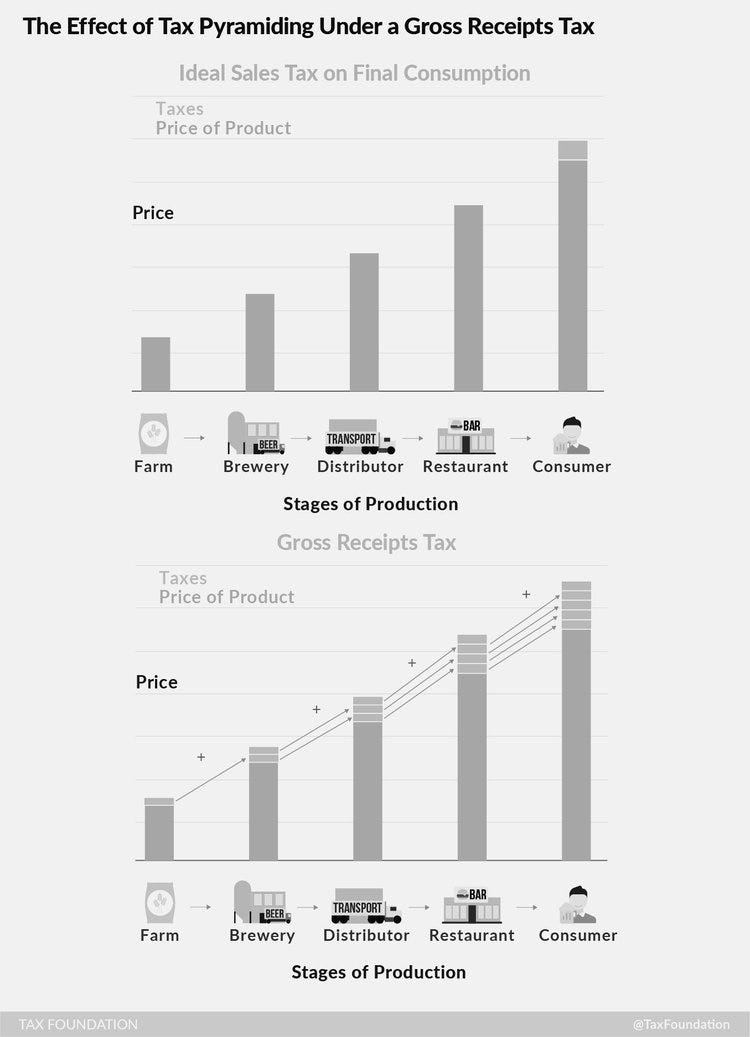

Sounds bad, right? Well, some of the other taxes Texas has are even worse. The Miscellaneous Gross Receipt Tax, Gross Receipts Tax on Mixed Beverages, Tax on Motor Vehicle Rentals, and Texas Franchise Tax, rather than taxing businesses based on their profitability, tax businesses based on their total revenue. Consequently, companies that have a lot of revenue but low-profit margins end up paying more taxes than businesses with meager income but far higher profit margins. They also, like sales taxes which hit business transactions, create a Tax Pyramiding effect, which can be visualized in the attached graphic by the Tax Foundation.

One bright spot in Texas tax policy is the severance tax. Severance taxes are taxes on the extraction of natural resources. As of 2018, Texas collected more severance tax revenue than any other state, bringing in around 5.2 billion dollars for the year. Presently, the severance tax is 7.5% on the market value of gas extracted, 4.6% on oil, and 4.6% on condensate (natural gas condensation).

Severance taxes are good for a few major reasons. First, they, in a fashion similar to land value taxes, capture value from a natural monopoly. Natural resources, like land, are the product of no human being. Therefore, it only makes sense that when they are captured by a private group, just compensation be paid to the rest of society for such an acquisition.

Second, various studies have shown that severance taxes do not have much of an effect on extraction. In a study conducted by Jason Brown of the Kansas City Federal Reserve, Peter Maniloff of Colorado School of Mines, and Dale Manning of Colorado State, the authors found that "the response to a change in tax paid per barrel of oil is inelastic." Put differently, the tax rate on oil extraction does not seem to have a major effect on the level of extraction. These findings are substantiated by various other studies, including this paper by the West Virginia Center on Budget & Policy. If this is true, it means that not having a severance tax up to a certain point is equivalent to leaving money on the table.

Third, Severance taxes, even if they were to impact extraction, would mostly be doing something positive. The act of capturing none renewal resources located deeply underneath the ground has many well-documented externalities. If it was to be proven that severance taxes do indeed reduce extraction, their existence would still be justified insofar that they were at a level that properly internalized extractions externalities (see Pigouvian taxes).

But just because severance taxes are mostly a good idea in concept does not mean that Texas's current severance tax policies are ideal. Right now, the state provides a litany of exemptions, deductions, credits, and other special goodies to certain businesses. These corporate treats are inequitable and negatively impact revenues. Additionally, there is a case to be made that the current rate structure is sub-optimal. Texas has had roughly the same rates since 1951. Present rates are not a reflection of in-depth economic analysis but rather a carryover from a past where information on the topic was far more limited than it is today. For this reason, some modifications are at least worth consideration.

B. Insufficiency

An additional issue with the Tax code is the relatively paltry amount of revenue it raises. Texas raises around 1800 dollars less per capita when compared to other states. This means less money going to schools, social welfare, and healthcare. The lack of crucially needed spending in these key areas is part of the reason Texas ranks 31st in healthcare, 34th in education, and 39th in upward mobility. In a country where the performance in all these areas is already pretty bad across the board, being in the bottom half of states is completely unacceptable.

This is occurring, all the while state debt is slowly growing and local debt is booming. In the years 2010 to 2019, state debt grew by 41%. But even with that growth, state debt is tiny in comparison to the gargantuan 365.3 billion dollars in debt held by local governments.

A significant cause of this explosion in local debt is the general decline of state funding to essential public services over the years. From the years 2007-to-2017, local spending per pupil rose by $990.21, largely due to inflation and what economists call "cost disease," meanwhile, state spending actually fell by $339. The shifting of this fiscal burden has left many school districts struggling with few options left other than selling bonds to cover the funding gap.

To halt the debt spiral, Texas needs to adopt tax measures that not only shore up revenues at the State level but also allow greater state aid to local services. This will improve their fiscal health and also come with the added benefit of decreasing the inequities in public service quality around the state

C. Regressivity

As of 2021, Texas had the 13th highest level of inequality in the United States, with the top 20% alone earning 51% of all the income in the state. This issue has only been exacerbated by the tax code. According to the Institute on Taxation and Economic Policy, Texas has the 2nd most regressive tax system in the nation, with low-income families paying an average of 13% total in state and local taxes and the rich paying a comparatively tiny 3.1%. It turns out, not only is the state’s fiscal policy failing to address rising inequality, but it is actually actively making it worse.

2. The Solutions

Luckily, when something is really broken, there are usually plenty of ways to improve it. Of first priority should be ending the gross receipts taxes. There is quite literally no reason for them to exist. For the little revenue they raise, they more than make offset themselves in terms of the economic harm they cause. Following that, the severance tax should be revised to end all the special deductions, credits, etc., and rationalize the rates in line with our contemporary knowledge. Other miscellaneous taxes on car rentals and hotel accommodations, among others, should be wiped from the books.

If we keep the sales tax, a good start would be redefining the sales tax base to include all final retail goods and services. Another common-sense reform would be to mimic and try to even surpass states like Idaho and Missouri in how comprehensively we exempt business-to-business transactions. Sourcing rules should be changed to follow destination sourcing norms as is most common around the country. It is also in the interest of Texas, along with all other states with sales taxes, to support federal policy solutions that would harmonize sales taxes across states and streamline enforcement.

If the many diverse nations of the European Union can coordinate their consumption tax policy, surely the United States can too! In the meantime, Texas ought to finally join the Streamlined Sales and Use Tax Agreement. The agreement, currently consisting of 23 states, already does a lot of the things federal legislation on the topic would do, albeit not as well. With these reforms, the retail sales tax would be in a much better place than it is today.

But, as I mentioned earlier, Texas doesn't just need to raise the same amount of revenue in a better way; it also needs to raise more revenue. Given this objective, it would be prudent for Texas to create a few new tax measures in order to generate greater positive cash flow. In this effort, a wise option is to boost and inflation adjust the tax on gas. Petroleum vehicles have plenty of externalities, and therefore it is only fair their users contribute extra to public coffers. As it stands today, the state gas tax is not even close to fully internalizing these externalities, and therefore, the state is justified in increasing it.

Another solid policy would be to create a Vehicle-Miles-Traveled tax (VMT). As already existent in two states, a VMT taxes vehicles based on the amount of damage they do to the road. It calculates this by looking at the vehicle's mileage, weight, and number of axles. Per common sense, a massive truck with 90,000 miles a year costs the public more in road maintenance than your aunt's seldom-used Toyota Corolla. In the sense that ultimately, public infrastructure costs are gonna come from taxation, it only makes sense that people pay in proportion to how much they benefit from the system. A VMT paired with a strengthened gas tax would discourage the purchase and the excessive use of unnecessarily large and heavy vehicles and would increase the de facto tax benefit for gas-efficient/electric vehicles. In this way, these taxes actually increase, not decrease, total economic efficiency.

Since VMT may be politically difficult, an alternative mechanism that would achieve a similar end is the expansion and modernization of tolls. At the moment, tolls don't discriminate between classes of vehicles, don't price congestion, and don't charge based on the length of trip. They also don't apply to the majority of highways in the state. By expanding them and embracing international best practices, we can raise revenue in a way that reduces congestion and puts mass transportation (trains, busses, etc.) on a level playing field with cars.

If policymakers are willing to be really ambitious, we could even consider replacing the gas tax with a more substantial and broader carbon tax. Several studies have outlined how state-level carbon taxes are both possible and have some benefits. Although, of course, federal action would be preferable.

Overall, tax policy in Texas, in contrast to its positive reputation, is actually quite poor. This is not due to a lack of options. A better tax code awaits the day voters and politicians become aware of how broken the status quo is and how clearly superior the alternatives are. For the sake of all Texans, let’s hope that day is sooner rather than later.