Principles of Effective Tax Policy

Better ways to tax

Taxes, taxes, taxes, we all hate them, and we all think that the current way the government raises them is unfair. In the United States, our almost endlessly spanning tax code as it stands today contains an innumerable number of harmful measures, needless complexities, and, dare I sound like every Democrat Presidential candidate ever, "loopholes."

All the while, political discourse surrounding the topic is remarkably un-invigorating. One side, namely the Republicans, continues to call for a more simplified and efficient tax system, and the other calls, rightfully so, for more progressivity in the tax code to combat rising wealth and income inequality.

Whether these rhetorical strategies are genuine is dubious, especially in the case of the Republican proposals, but the point still stands that the issue is presented in a completely dichotomous fashion. A voter may be forgiven for thinking that there is a directly proportional trade-off between the two values, both efficiency and equality.

This is not the case. As I will show, a tax system that is massively more egalitarian and efficient is totally within our reach, given that we have the political will to realize it. The following sections will cover a concise list of tax types suitable to replace all existing measures while still being capable of raking in an equal or even greater level of revenue than is raised presently.

I. LAND TAXES

Case

There is a commonly referenced Benjamin Franklin quote that states, "In this world, nothing can be said to be certain, except death and taxes." Ignoring the fact that for many billionaires, that last part is not so certain, it is reasonable to say that land is quite unavoidable as well. And I don't mean just land in the sense of the surface of planets. I also mean land in the more comprehensive sense as consisting of everything emerging from nature, including our rivers, natural resources, etc.

These things are all quite hard to escape, and importantly for this discussion, all necessary elements of the production process. In addition, since no person creates or has created land, it actually represents a unique case in which taxation does not inhibit overall economic efficiency.

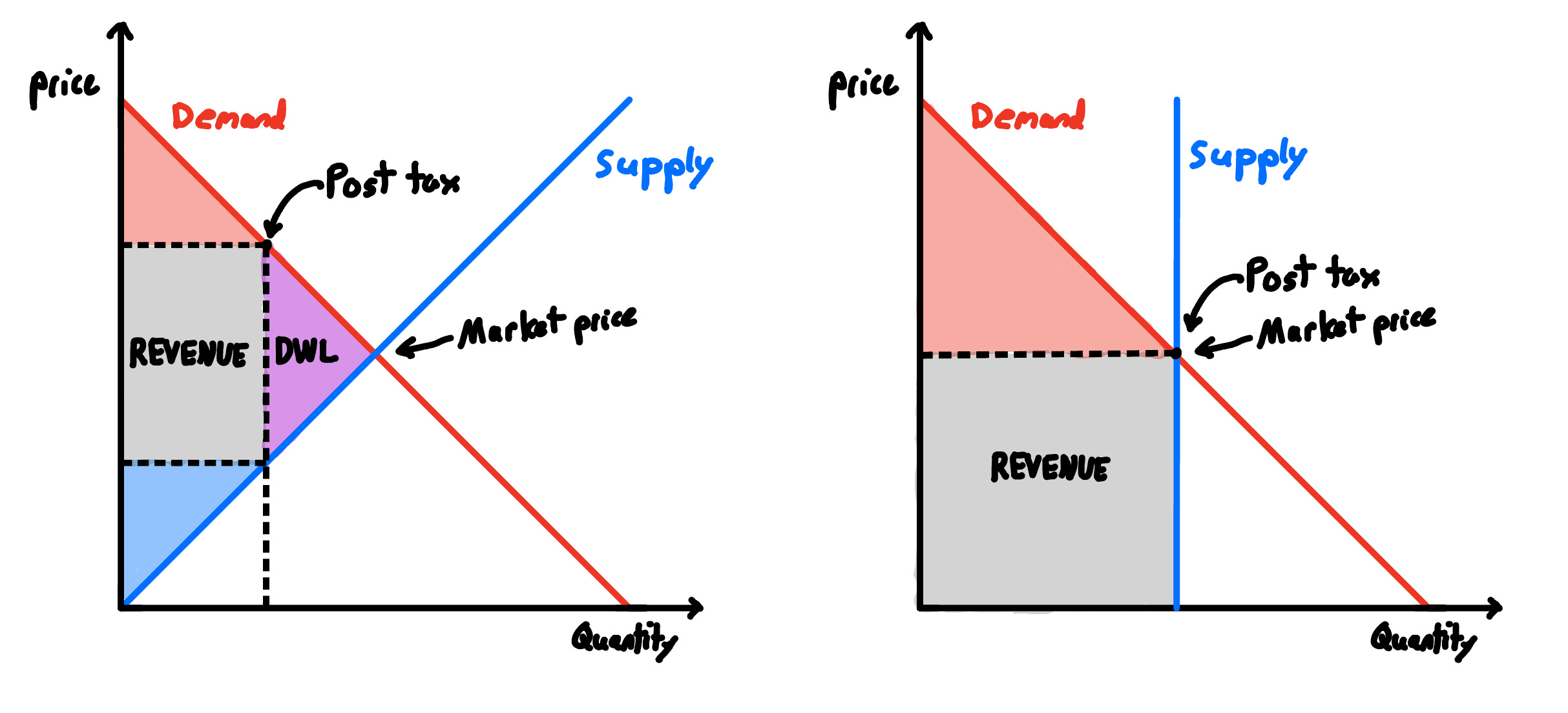

See, unlike other things in the economy, when you tax land, you don't get less of it. No amount of taxation will make Florida disappear, even if that might be a good thing. So theoretically speaking, the public can have a tax rate on land as high as it wants with no consequences.

Land is in fixed in supply, so no matter how high the rate gets, its sale value will drop proportionally in order to reach equilibrium, i.e., a price where each parcel of land is being used. Hidden here is where the other benefit of LVT is; not only does it raise revenue in a way that seems quite intuitively just, but it also forces land users to be more effective in how they use their land.

To illustrate this, let's analyze some of the poor behaviors that occur today. Take three landowners:

Bob owns an empty parcel of land,

and Dan owns land and plans to develop it.

Bob, in the current system, can make substantial profits by doing absolutely nothing. This is because, as incomes go up, the value of land also goes up as well. Thus, Bob does not have to contribute any value at all in order to make out quite well for himself in the economic framework we have today.

Dan is being productive, but he doesn't have to be. If he wanted to, he could act like Bob and devote his energies to other endeavors.

Now let's take a Land Value Tax world. In this world, every Land Owner has to pay 100% of the rental value of their land to the government periodically. This means that as land values go up, so too would the passive cost of owning it. Bob would be in a complete bind because he is very unproductive with his land and thus is generating no revenue from it. This would leave him with a choice, either become productive like Dan and use his property to its fullest potential in order to be able to continue affording it or sell it off to someone else who will. Either way, the public wins. Landowners are more productive with their land, and the public get's a large amount of revenue to spend.

If this seems like it's too good to be true, it's not! It turns out that the general academic consensus agrees that this would be quite a solid way to raise public revenues. People all over the political map have endorsed the policy, including but not limited to Winston Churchill, Abraham Lincoln, Milton Friedman, Yanis Varoufakis, Albert Einstein, and an almost endless list of others. And it's not simply a theoretical proposal either; forms of Land Value taxation already exist in some American cities and in countries like New Zealand, Denmark, Singapore, and Taiwan.

If you are interested in learning more about the policy, I encourage you to read this policy paper here. There is also a wonderful Reddit you can find at r/georgism, which is full of nerds that are willing to answer any and all questions you have relating to the policy.

Land taxes need not only apply to land in the conventional sense. The same idea holds true for resource extraction and the use of other common goods. Land value tax already hits resource rents below the ground, but for the coasts and publicly owned land or lakes, market-based extraction rights or licensing can achieve the same end.

New Zealand's Individual Transferable Quotas for fishing show one way this can work. Spectral auctions for the purchase of radio waves show another way. What is important is, insofar as someone is yielding for monopolizing a gift from nature for themself, they can be made to compensate the public for its loss.

II. PIGOUVIAN TAXES

Case

As any Econ 101 student will tell you, many activities that we engage in as individuals have costs that affect other people. Sometimes these costs are so negative that it justifies making an individual decision illegal. For example, it is illegal for me to purposefully burn down someone's house, and it is illegal for me to dump toxic waste into a river.

In both these cases, a private decision I make significantly harms other people. But what about a situation where my decision harms others but not so significantly extent that we want to make it illegal? Well, that's where Pigouvian/ externality taxes come in. These mechanisms seek to raise public revenue and enhance private decision-making efficiency by internalizing the externalized costs of an action.

Let's look at how a Pigouvian tax would enhance a private decision compared to the status quo. A company today, say Barnaby's Bakery, is trying to choose what electricity provider they should use.

One provider uses fossil fuels to generate electricity and charges 10 dollars for every unit of electricity. Since they use fossil fuels, they also cost society an additional 3 dollars, making the total cost of each unit of electricity they provide 13 dollars. Another provider uses solar panels to generate electricity and charges 12 dollars per unit. In the status quo, Barnaby's bakery would probably choose the fossil fuel company over the green energy company because their price is a full 2 dollars less. But if a Pigouvian tax system was in place, in this case, a Carbon tax, the opposite decision would be more economical.

But a Carbon tax isn't the only example of this type of policy; there are other proposals worthy of consideration, including a weighted mileage tax and a tax on "sins," in this case meaning unhealthy products such cigarettes, alcoholic drinks, and sugary foods. A new tax code would be wise to include as many of these types of taxes as possible, given that administering and enforcing them is not too arduous.

III. CONSUMPTION TAXES

Case

Under the present tax code, people are taxed on their income six times via capital gains taxes, income taxes, inheritance taxes, corporate taxes, employee-side payroll taxes, and employer-side payroll taxes, and on their outlays three times via gift taxes, estate taxes, and sales taxes. If such a large number of taxes were being employed, all with their own separate justifications, such a system could be forgiven, but that is not the case. Many of these taxes are completely redundant; others cause harmful distortions in behavior. Thus for the purpose of generating revenue, I pose an alternative, instead of taxing people multiple times when they get money and when they use it, we tax them when they use it. This brings with it many advantages.

Consumption taxes do not discriminate between investment and labor income, thereby encouraging greater savings and making administration easier. This may seem subtle, but it's actually very important. See, right now, our system taxes people twice when they get their paycheck via income tax and payroll taxes, then again when they get capital gains. Not only is this pretty difficult because taxing people's illiquid gains on investment is admittedly hard to enforce in an economically sustainable way, but it also provides a double tax effect that reduces the desire for people to save. Taxing the use of money instead of the gaining of it allows us to tax both capital income and labor income indiscriminately in a way that's easier for the public to enforce and encourages more people to save.

Consumption taxes are great because they target the aspect of inequality that matters most, inequality of consumption. When we look at the tremendous riches of people like Jeff Bezos, what's most aggrieving is not the dollar amount of their net worth; it's how they use that money to live lavishly, with mega yachts, super mansions, and ludicrously expensive cars. It is upsetting to think that the amount they spend on ludicrously expensive consumption (including political donations) could have been used to transform the material standard of living of many poor and working-class individuals. When consumption is taken out of the picture, the practical problem of remaining inequality becomes far more opaque. If the biggest reward for earning a higher income was the capacity to determine what charity that income goes to, would inequality of income really be so bad?

Now that I have enumerated these advantages, let's briefly touch on their implementation. My ideal model would be a combination of Value Added Tax (VAT) with an X Tax. VATs are useful in the respect that they are immensely efficient, extremely hard to avoid, require no filing by the average person, and are paid by consumers regardless of their legal status or residency. The ideal VAT rate would be in the 10% range and would encourage state and local governments to end their sales taxes and instead incorporate themselves into the broader VAT (or end them entirely and gain revenue from a land value taxation sharing arrangement).

Meanwhile, an X tax would be able to hit this exact same base, except with a progressive bracketed structure (which is very helpful politically), and in a way that actually doesn't increase the price level. To learn more about the X tax, read this: The X Tax: The Progressive Consumption Tax America Needs?

And that's it. The conceptual basis for an entirely new code; feel free to spam this hyperlink when people ask you for pay fors. I hope that after reading this, you realize another world of taxation is possible. We are not faced with a choice between equity and efficiency. We can and should have a tax system that does a hell of a lot more of both!

“Taxpayers of the world unite; you have nothing to lose but your need for a tax lawyer. ”

— Probably Marx