A Novel Path to Healthcare Reform

Less insurance more competition

In a previous piece, I outlined a pragmatic plan that would put the American healthcare system on par with many of our OECD contemporaries. Through a series of reforms, the American healthcare system can be brought up to international standards with rationalized prices, reduced waste, and greater access.

But maybe having a system simply on par with other developed nations shouldn't be our objective.

After all, other country’s healthcare systems have many problems of their own. All around the world, costs are rising, providers feel overwhelmed, and wait times leave many frustrated. The OECD estimates that “Health expenditure will outpace GDP growth over the next 15 years in almost every OECD country.” The status quo has left journalists, academics, and politicians alike looking aimlessly at their neighbors for reform because the current trends seem so unsustainable.

So what is it that no one has figured out? Besides demographic changes and the rise of new expensive treatments, which both push up costs, much of the current crisis has to do with a lack of productivity growth.

Healthcare has never been a sector with the greatest automation. While medical innovations have created many life-changing treatments and drugs, they have seldom reduced the costs of basic services like primary care, specialty care, MRIs, CT scans, and the like. On the contrary, these costs have continued to rise, often at a startling pace.

A key aspect of this is the severe lack of labor saving technology adoption. Many medical services are just as labor-intensive today as they have ever been before. In fact, partially due to the rise of insurance in the United States and other OECD nations, services have become much more labor intensive because of the more significant billing and negotiation demands that accompany third-party payments.

When a sector's productivity stagnates, prices are inevitably driven up, as growth in other sectors necessitates economy-wide wage increases. This is called the Baumol effect, and it's been a central factor plaguing healthcare systems all over the world for decades now, well, except in Singapore.

A Glimmer of Hope

According to Singapore's Ministry of Health, between 2007 and 2017, the city state's average annual healthcare inflation was 2.6%, only 0.3% higher than general inflation. This meager cost growth is especially impressive, considering that life expectancy jumped by nearly three years over the same period.

Even better than the slow cost growth is the fact that their healthcare spending sits at just above 4% of GDP, despite having a GDP per capita not too far from the United States and Switzerland, which spend 18.3% and 11.29%, respectively. They manage to do this while leading the world across various health benchmarks like infant mortality, maternal mortality, and disability-adjusted years.

Wages for medical professionals can only explain a portion of the difference. On average, a General Surgeon in Singapore earns 265,881 USD as compared to 388,384 USD in Switzerland. If wage differentials were the only factor we would expect their system to cost approximately 31% less than the Swiss, not 65% less! Wage differences also wouldn't explain the huge gaps in cost growth unless labor input cost growth was very different between the two nations.

So, what has been the secret sauce to Singapore's model? There are many elements, but what most differentiates their approach from the others seen in the OECD is their focus on fostering competitive markets for medical services through limits on insurance, price transparency, and reference pricing.

For those who like to get a more comprehensive understanding of their system, I highly recommend reading Affordable Excellence.

[1] Taking third-party payers out

In Singapore, they treat health insurance a lot more like car insurance. In the same way that car insurance wouldn't pay for routine maintenance, car washes, or new windshield wiper fluid, health insurance in Singapore is reserved for only unexpected, large costs.

Many care services, including family medical care, minor surgeries, statutory medical checkups, health screenings, x-rays, and various specialty care, are left outside of the public insurance system to be funded out of pocket.

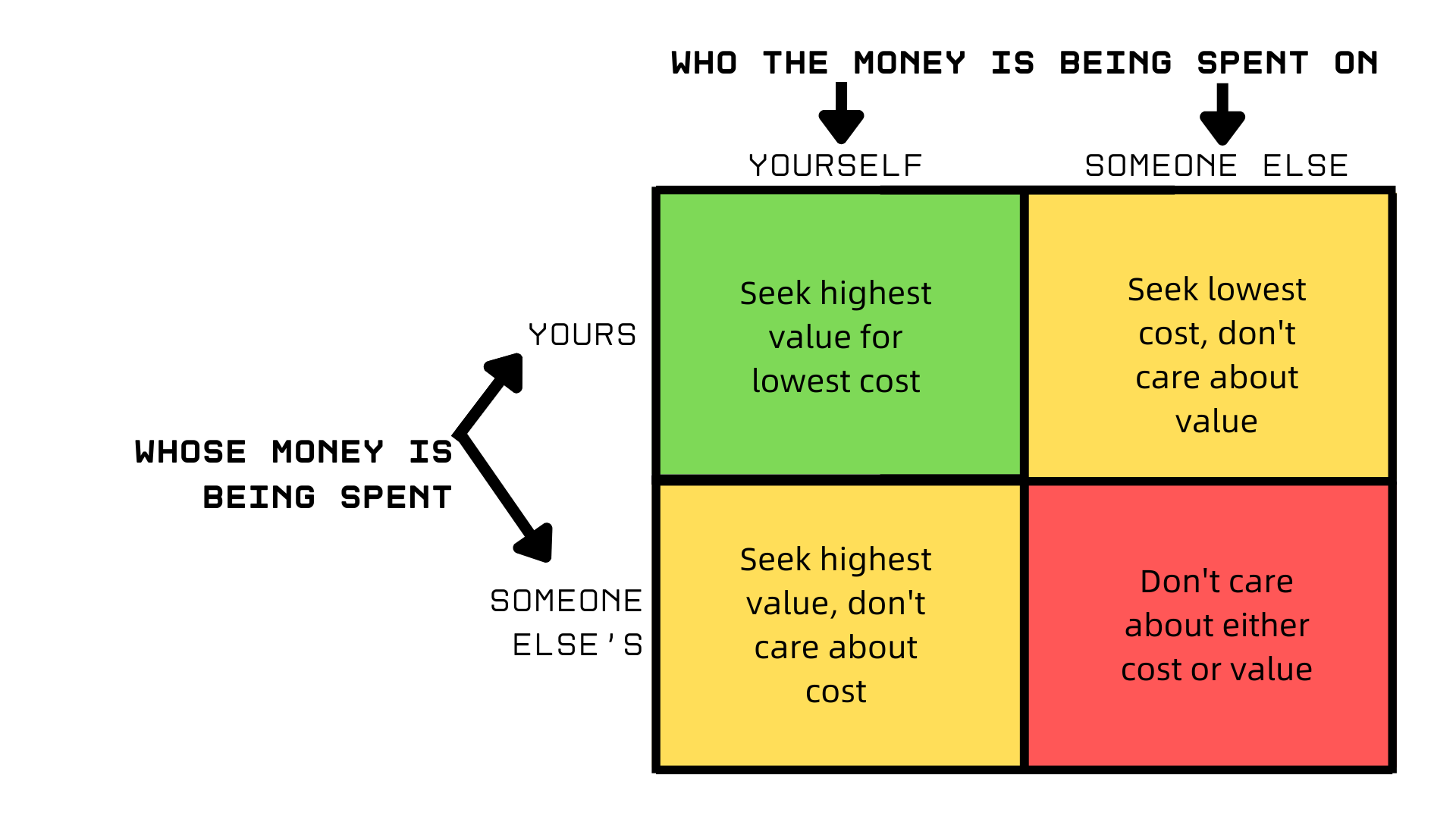

This has proved to be an exceedingly beneficial choice. In many cases, insurers are middlemen that only add complexity and worsen incentives. They force providers and administrative staff to spend an enormous amount of time ticking boxes, coding payments, and negotiating prices. Furthermore, since they cover such a large portion of the bill, consumers are made mostly indifferent to price, eliminating the capacity for price competition between providers.

As of 2023, in the United States, 563,366 people are working at health insurance companies and many more thousands at providers for the primary purpose of dealing with the immense complexities relating to third-party payments. In the end, such a broad area of insurance coverage adds 100s of billions of dollars of unnecessary cost to the system in administration alone.

A key part of Singapore's model is stripping back the reliance on these insurers, removing the intermediaries where they are unnecessary.

[2] Price Transparency

With the role of insurance drawn back, providers have a renewed incentive to publish their prices and engage in competition.

This means that, for the first time in a long time, there is actually a compelling reason for providers to cut costs by switching to more cost-effective treatments and eliminating unnecessary labor.

But the government hasn't just been content to let providers sort the price publishing out; they have made deliberate efforts to deepen this competition. For over a decade now the government has required that all hospitals list their prices publicly. In addition, they have provided a fee benchmark to serve as a reference database for both consumers and providers alike to get an understanding of how much a specific service can be expected to cost.

This has not been without impressive results. In 2004, the price of a LASIK surgery was 2,300 Singaporean dollars. By 2008, that price had been reduced to only 1,400 dollars. Notably, LASIK prices have also fallen in the US in large part due to its ineligibility for insurance coverage.

In Singapore, a similar story has been true for a litany of other procedures, where prices have been contained if not depressed by the market mechanism.

Comparisons to the United States highlight their approach’s immense superiority. While a heart bypass surgery in the United States will set you back, on average, 123,000 USD, in Singapore, you can expect to pay just 27,083 USD. Knee replacements also cost less, 72% less to be exact. The same story is true for C-sections, cataract removal, appendectomies, tonsillectomies, and virtually every other procedure.

Price transparency is something that not only has been shown to work in Singapore; it's also worked in the United States. For plastic surgeries, where prices have always been relatively transparent and most payments are covered out of pocket, costs have consistently gone down in inflation-adjusted terms.

A study by the American Enterprise Institute found that in the period 1998 to 2018, plastic surgery prices rose a full 19.7 percentage points slower than inflation. Over the same period, a few procedures even fell in inflation unadjusted terms, from botox injections by -26.7% to laser hair removal by -47.3%.

[3] Doing Insurance Correctly

Insurance is complicated, and Singapore has operated under the philosophy that less is best. Yet, for catastrophic costs, it is a necessity. The vast majority of people cannot afford to pay for chemotherapy out of pocket, let alone the enormous costs that come with end-of-life care.

For these tasks, the government has resulted to the simplest of solutions, direct provision.

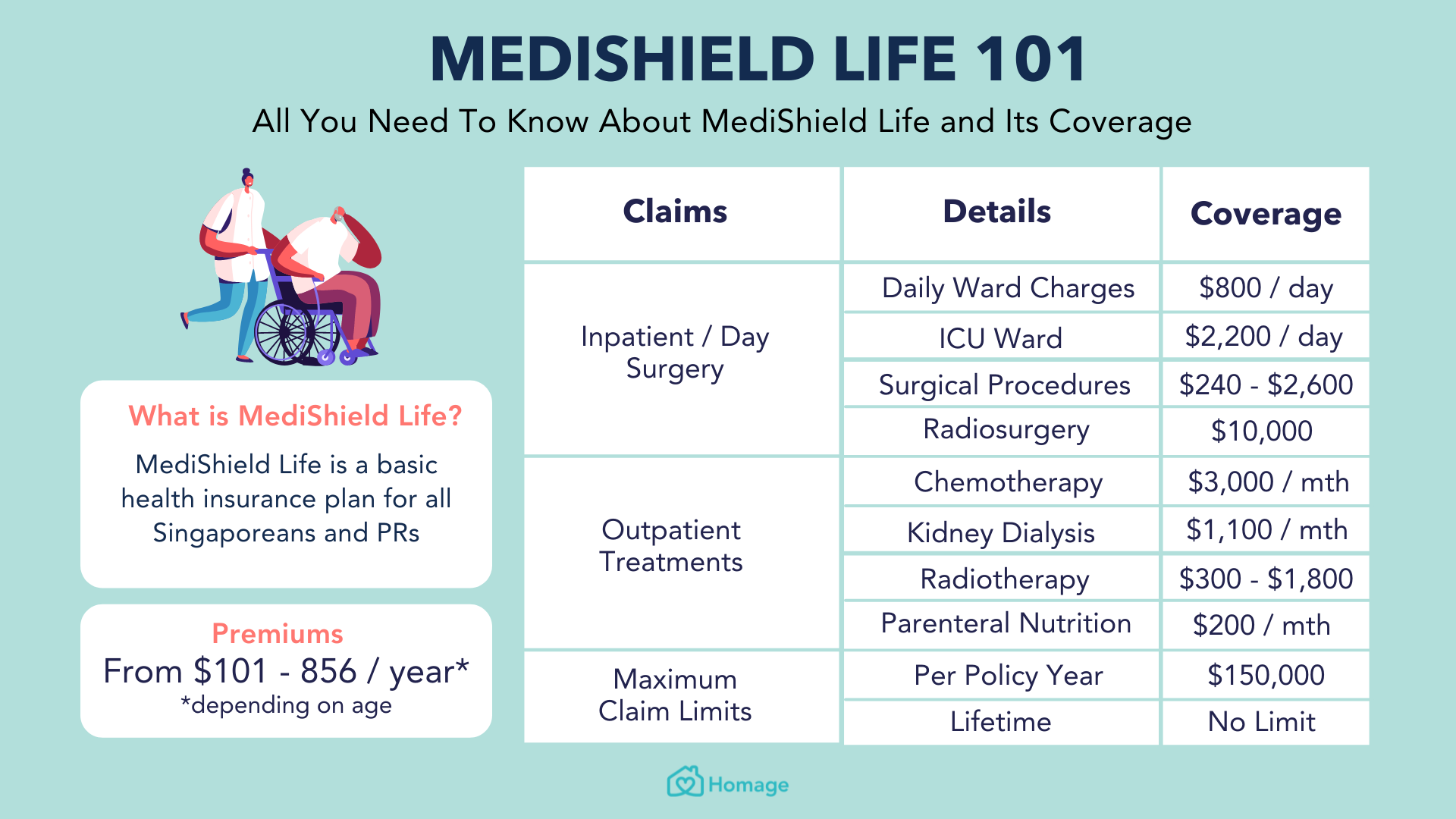

Since 2015, all citizens have been automatically enrolled in a catastrophic public insurance program termed MediShield Life. This program, unlike many American "catastrophic” plans, only applies to expenses that are non-routine, and sufficiently out of the ordinary. This includes emergency room visits and very expensive medically necessary surgeries, among a short list of others.

Yet even where MediShield does kick in, cost sharing remains. Patients only get coverage once they meet their deductible, and past that, they pay 10% of the bill until they hit their yearly maximum.

A portion of this cost-sharing can come out of mandatory tax-preferenced savings accounts that operate similarly to Health Savings Accounts (HSAs) in the United States. Although these savings accounts have one key difference, contributions to them are mandatory.

Fascinatingly, even Surgeries and expensive therapies that are covered by insurance remain exposed to the price mechanism. This is achieved via reference pricing, whereby the government determines the maximum amount of money it will put toward a specific service, and then the patient is left to price shop from there.

If they decide to go for a surgery that is more expensive than MediShield has outlined, they must pay the difference. If they go for a cheaper one, they will receive a portion of the savings by no longer being on the hook for as much coinsurance.

This allows price competition to stay around even for costly procedures.

For care that is not catastrophic in nature but still cost-prohibitive for either the poor or those with chronic conditions, additional subsidies have been put in place. These include direct subsidies to chronic care providers, an extra assistance program called Medi Fund for the poor, and cash payouts to the disabled.

The confluence of these various policies, combined with a forward-looking government that has enforced strict competition laws, taken measures to minimize excessive provider risk, ensured an adequate supply of physicians and made crucial investments in centralized patient databases and telehealth, have come together to create a world-class system, at an extremely cheap price.

The following section will be about how the lessons of Singapore can be applied to the American context to get us a system that not only is on par with other OECD nations but could conceivably surpass them in many respects.

Direct Primary Care

As Singapore shows, and common sense reveals, there isn't a good case for insurance in primary care. Primary care needs are relatively static, so there is practically no reason insurance, which only exists to help minimize risk, should be involved in the process.

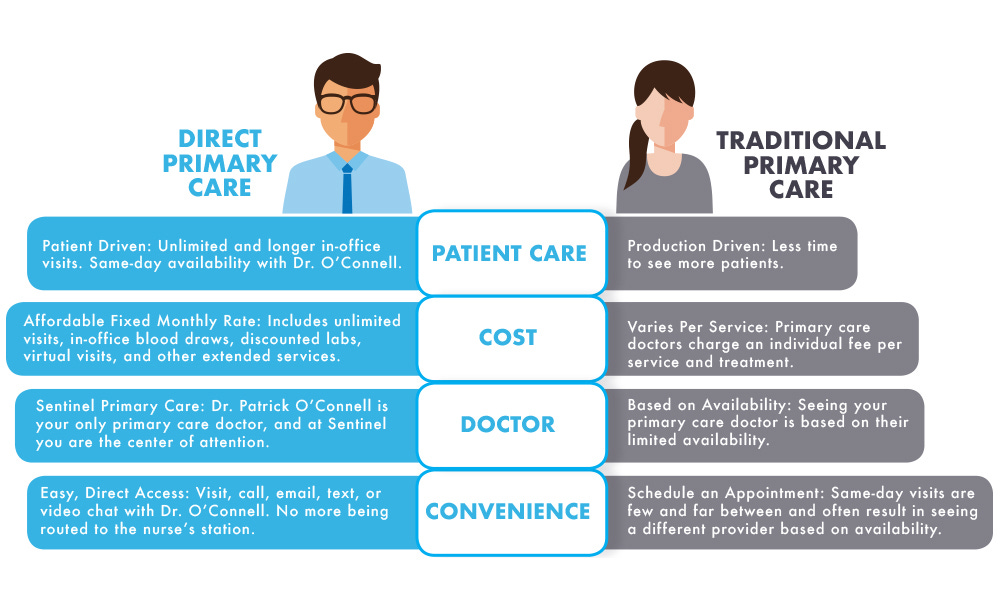

Luckily, progress towards removing them from the system is already well on its way in the form of the growing movement for Direct Primary Care (DPC). Starting in 2007, tens of thousands of frustrated physicians abandoned the insurance system in favor of direct payment.

In place of the typical fee-for-service payment model, many of these physicians adopted a subscription-based system, not too different from Amazon Prime or Netflix. In exchange for around 75 dollars a month, patients are granted unlimited primary care services, including checkups, disease management, wellness coaching, and even minor surgeries.

This has brought with it many benefits. The cost savings from eliminating insurance allows providers to care for a far smaller panel of patients. While the typical General Practioner sees around 2500 hundred patients, the typical DPC GP only has to care for 300-700.

At first glance this might seem to indicate a reduction in productivity, but the opposite is actually the case. Fewer patients mean longer visits and the capacity for 24/7 open lines of communication and deepened patient-provider relationships.

In practice, this means a more effective primary care system that can improve outcomes and create savings in other places, both things that America is sorely in need of.

As of now, over 50% of family physicians spend 16 minutes or less per visitation. Short visits and poor incentives lead to GPs outsourcing their work to expensive specialists and writing an excessive number of prescriptions. Americans pay the price, both in their premiums and with their lives.

In 2020, a study by the Lown Institute estimated that medication over-prescription would lead to over 150,000 additional deaths by 2030. They also found that an average of 750 over 65 Americans were hospitalized due to the side effects of medications every single day.

In the DPC model, these issues are largely averted, and the reduced need for administrative staff makes it such that while there is a more favorable patient-to-physician ratio, there is actually often a decline in labor intensity.

99% of DPC physicians report having better overall satisfaction, and 98% report feeling they are much better able to provide "quality primary care." This is unsurprising; more stable revenue leaves them in a far less precarious financial position. Additionally, the improved incentive structure from ditching fee for service allows them to focus on proactively promoting the health of those they serve instead of having to constantly put out fires as they arise.

The data, albeit limited due to DPC’s relative youth, has been generally positive. A study by the Society of Actuaries found that those who opted for DPC saw a 40.51% decline in emergency department utilization and a 19.9% reduction in hospital admissions.

But direct payment need not be exclusively used for primary care. People who need to frequently see cardiologists and or endocrinologists due to chronic health conditions might also benefit from the subscription model. Other specialists like psychiatrists, dermatologists, podiatrists, and obstetricians would also benefit from disconnecting themselves from the insurance system.

A world of Direct Primary Care is one where price finally matters again, just like it does in Singapore. Providers, now in genuine competition, have to try to one-up each other not only on quality but also price. The practices that provide the best bang for the buck will get the most enrollees; those who don’t will be forced to adopt better practices.

Ultimately, patients get what they are in such deep need of currently, inexpensive, quick care tailored to their health needs by physicians that have the time to solve problems at their roots.

Universal Catastrophic Coverage

But DPCs aren't a silver bullet. Primary care is only 5-7% of healthcare spending in the United States. Even if it was expanded in such a way so as to reduce healthcare spending within other categories and specialist care, too, departed from the insurance system, the need for some form of insurance for the remainder of healthcare spending would be intact.

The best method would be to copy the MediShield approach and embrace Universal Catastrophic Insurance. Direct government provision is helpful because getting markets in health insurance correct is quite difficult, as I’ve covered in this piece; furthermore, even if the issues with private insurance were to be ameliorated by adopting foreign best practices, research has indicated that markets will still remain somewhat dysfunctional.

A study by Economists from Harvard and the University of Michigan found that:

“When workers at a private employer were offered a choice of health plans that included a dominated (inferior) plan, a significant portion chose the dominated plan.”

The results, which have since been confirmed by subsequent studies, paint a bleak picture for Managed Competition. It appears that consumers are unable to make rational choices even between an extremely limited number of options.

Ultimately if America switched to catastrophic insurance, there would be little point in keeping private insurance for anything but supplemental coverage around.

Under UCC, people would be insured on only big-ticket items like treatment for chronic diseases, hospitalizations, and medically necessary surgeries. Premiums would be income-based (effectively a flat tax on wages), and deductibles/coinsurance would be the same for everyone. The administration would be done by the government in the same way that Medicare is administered, although, as mentioned, the breadth of coverage would be far narrower.

Crucially though, the payment method would need to depart from the current model used by most insurers. Instead of the cost of procedures being determined by central negotiation, provider prices should be set by the market. If one provider finds a cheaper way to provide surgery, they should be rewarded for doing so.

Just like in Singapore, this can be achieved via UCC using reference pricing for all nonemergency procedures, services, and drugs. Under this payment system, patients would have a set budget to meet the specific healthcare needs they have been prescribed and would be liable if they exceed it. Since there will be some coinsurance as well, there will also be an incentive to even leave some of the budget remaining if a cheaper option is found.

For drugs, this will mean the government will provide a level of support sufficient to pay for the most cost-effective medication, leaving it to consumers if they think more expensive name brands are worth the price.

To a limited extent, reference pricing has already been experimented with in the United States, and the results are confidence-inspiring. A study on an organization called RETA Trust found that a switch to reference pricing yielded an average savings of 14%. Meanwhile, research by the American Academy of Actuaries estimated that a national rollout of reference pricing could reduce spending on shoppable services by up to 28%.

UCC allows us to retain the best part of insurance while organizing it in a way that minimizes administrative costs and keeps the market, which is so necessary for productivity growth, intact.

An added benefit is that UCC, wouldn’t even necessarily imply higher taxes. The government is already responsible 49% of all healthcare expenditures, not even including tax preferences which further subsidize the cost.

Substituting UCC for current programs could easily be done in a revenue-neutral way, by redeploying funding coming from existing programs like CHIP, Medicaid, Medicare, the Employer Insurance Deduction, ACA subsidies, and the like.

Health Savings Accounts

Yet UCC alone may be insufficient. A large bulk of healthcare expenditures will be on things that aren't covered. Costs from coinsurance and deductibles may still leave care inaccessible, especially for the poor. To expand access and ensure people spend an adequate amount of money on preventative care, the government could universalize health savings accounts just like they do in Singapore.

In a similar fashion to social security, everyone would have an HSA automatically created for them. Deposits could come in multiple forms. One idea is a universal basic deposit. This would provide a monthly deposit for all citizens of healthcare-specific cash. Since this cash would be limited to healthcare spending, citizens would have no reason to skimp on regular screenings and primary care visits.

Ideally, such a program would be funded by a broad based tax on consumption. But an alternative proposal may be more politically favorable. Instead of making deposits universal, they could be financed by an employer and employee contribution (a capped payroll tax). Every worker would pay into their account up to a certain amount, with poor people getting a certain basic amount guaranteed. The amount of subsidy one would receive could phase out with income, somewhat like a healthcare money negative income tax.

This would make the cost of the program appear smaller and ease the transition. Employers who are currently required to provide insurance could be made to instead deposit some of the money they are spending in HSAs. While the difference would be mostly optical, and the mechanism slightly worse than universal deposits, optically, such a policy would be an easier pitch to politicians.

In reality, any such transition to uproot the insurance industry will no doubt face steep opposition. Yet, unlike Medicare for all, it will probably garner less resistance from providers, who will enjoy the idea of being somewhat liberated from insurance, both private and public alike.

Healthcare is complicated, and no one article could cover all the ways we can make it better. There are many regulatory issues that produce additional costs in the system. Changes to the FDA, licensing procedures, and liability, among various other reforms, would no doubt bring down the cost. In addition, the American system contains many unique deficiencies relating to insurance that only make matters worse.

But even if all these problems were solved, the fundamental dilemma would remain: low productivity growth. The best way to make inroads against this issue seems to be through markets. The issue is that well-functioning markets require consumers to spend their own money rationally to get the best value for it. Insurance in its current form precludes that possibility.

Singapore shows that inroads against cost disease can be made with smart government policy and the deep integration of price signals and competition within healthcare. It also shows that these ends can be achieved without abandoning the needy to suffer without care.

If the United States wants a system that not only catches up to our peers but also surpasses them, Universal Catastrophic Coverage, Direct Primary Care, and Health Savings Accounts for all show a promising path to that destination.

A healthcare system that provides higher quality and greater access at a more affordable price is within our reach; all we need is the political will to secure it.

https://assets.aeaweb.org/asset-server/files/9442.pdf

Have you not read Kenneth Arrow?