Fulfilling the Promises of Obamacare

Universal Healthcare in Freedom Land

The day is March 21st, 2010. After nine months of backroom deals and arm-twisting, the Affordable Care Act has been passed. American healthcare is finally going to be fixed, with universality ensured, affordability guaranteed, and health outcomes raised to global standards, or so we hoped.

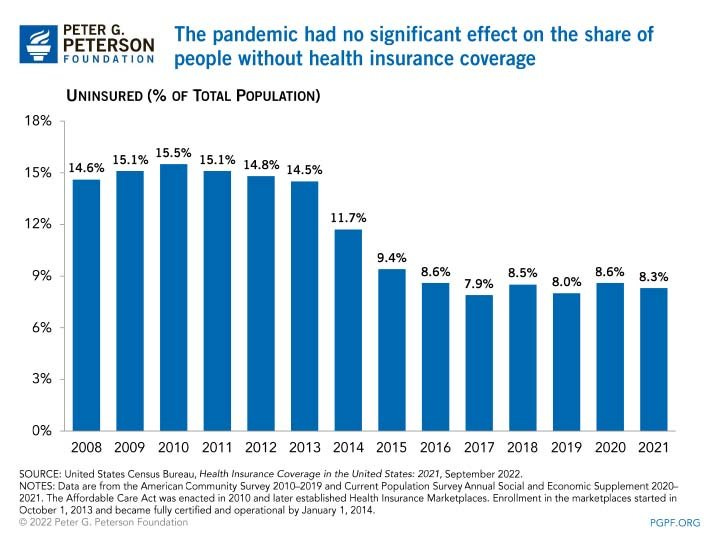

Despite the many laudable efforts the ACA made, there is no doubt it has fallen short of giving us a well-functioning healthcare system. 13 years later, 8% of the population remains uninsured. Even worse, the Common Wealth Fund has found that "people in the United States experience the worst health outcomes overall of any high-income nation.” We Americans have the lowest life expectancy of our fellow developed peers, the highest death rates from preventable diseases, and the highest maternal and infant mortality, and for this unique dishonor, we pay $12,914 per person.

1. Diagnosing The Problem.

(a) Costs

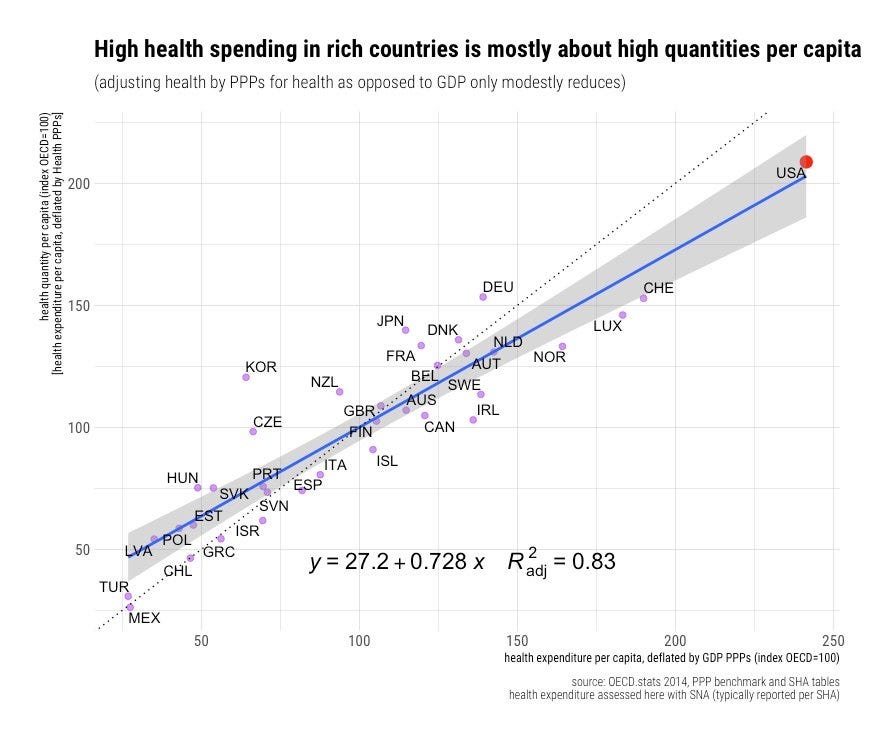

We have all heard that America spends twice the OECD average on healthcare. But why is that? Some have assumed the position that this additional spending can be explained by inefficiencies in our current system, but that isn't the whole story.

One of the leading causes is the fact that Americans are much less healthy than our developed peers, and this is mostly not the fault of our healthcare system.

We eat too many hamburgers and slouch at our desks too long. We get into more car wrecks, catch more STDs, are more likely to succumb to drug and alcohol abuse, and find ourselves more frequently being victims of violence.

To try to compensate for all this, we demand a greater quantity and greater intensity of care. Americans get more C-sections, knee and hip replacements, coronary artery bypasses, angioplasties, CT scans, and MRIs. We also take more drugs and get prescribed newer ones.

Our prices are indeed higher than in other nations, but that is mostly because we are richer. Any sector which is very labor intensive in a growing economy will inevitably experience the Baumol effect or, as it's often referred to, cost disease. Cost disease occurs as productivity gains in some sectors cause wage growth in others, even when those others have made no productivity gains. This effect leads to inevitable increases in the price level of medical services so long as healthcare maintains its high labor-intensive status.

The fact that our prices are higher than our fellow western nations should not be surprising; we have far higher incomes. Importantly, though, healthcare prices have grown significantly slower than real incomes, and so on average, if quality and quantity were held constant (they certainly aren’t), healthcare has actually become more affordable over time.

Unfavorable demographic trends are another explanation for America’s healthcare woes. Americans are getting older on average, and like the rest of the developed world has been learning, that has costs. Older people require much more care on average, so as the population ages, more healthcare spending is inevitable. That is unless we follow the peculiar advice of one Japanese professor and start convincing the elderly to commit seppuku (ritual suicide) en masse.

These facts should clarify that while there are big savings in healthcare to be made by cutting down on administrative costs, reducing unnecessary procedures, and eliminating barriers that delay treatment (thus increasing the severity of conditions), healthcare spending cannot be reasonably lowered to that of other OECD nations, and spending will continue to grow at a rate faster than GDP over time.

(b) Outcomes

As previously explained, Americans are very unhealthy, which can only partially be explained by our system. Efficacy for treatments is quite high, with Americans having lower than average hospital readmission rates and faring very well in cancer, heart disease, and stroke survivability.

The main issue as it pertains to the healthcare system is the lack of access on behalf of the uninsured and underinsured. Because of gaping holes in the social safety net, many Americans are forced to forgo treatment, contributing to our bad outcomes on various benchmarks like our high avoidable mortality.

(c) Affordability

The biggest tragedy of the American healthcare system is how many, by virtue of our insufficient social support, get locked out of it. The fear of emergency room bills and the looming sum of medical debt prevents many lower-income people from getting the healthcare they need.

While the other two problems can only be addressed by health policy to a limited extent, this final piece is entirely determined by health policy choices, choices that can be changed.

2. Single payer or...?

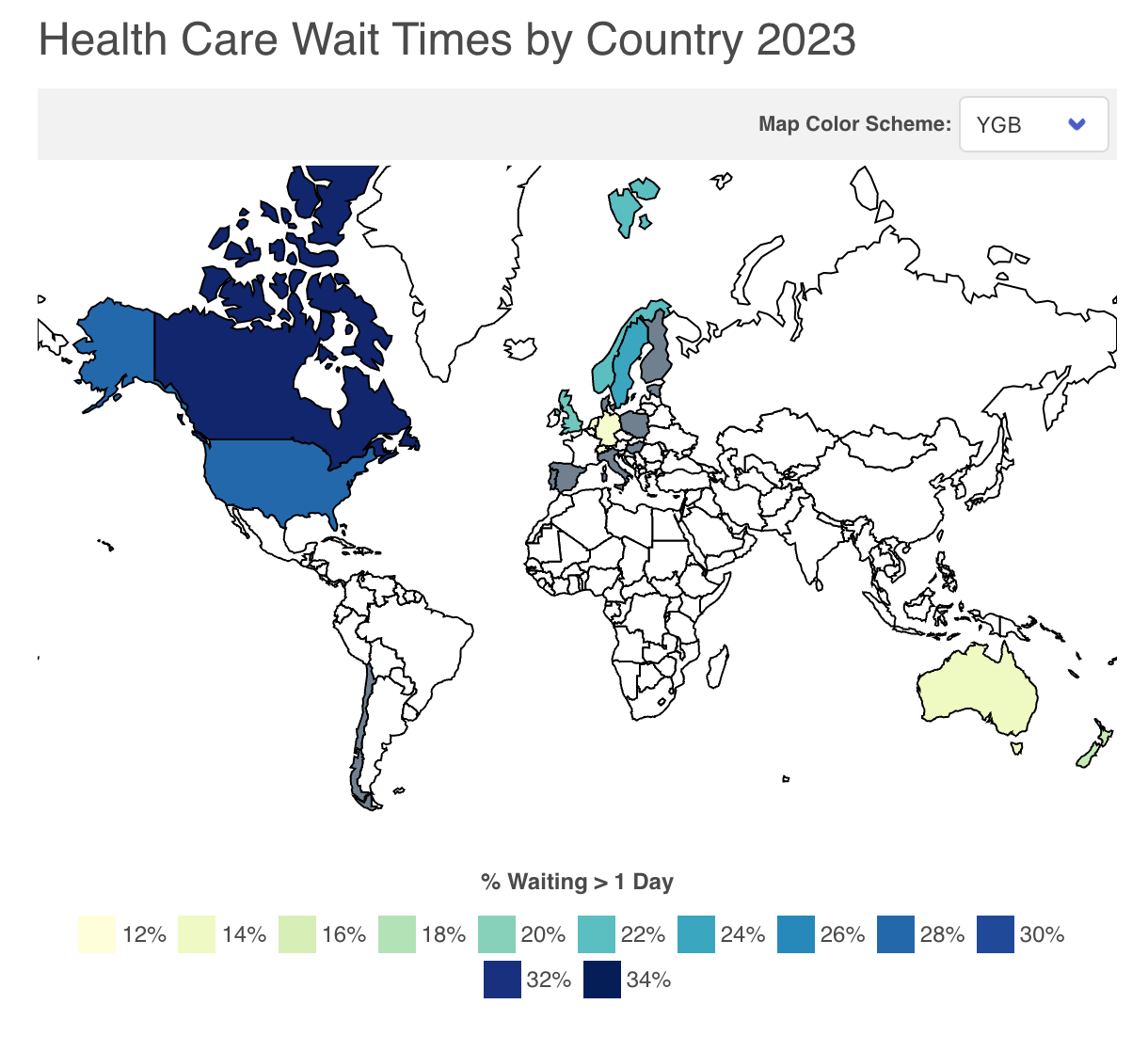

Obamacare set out to push the United States towards the Managed Competition model employed in countries like Switzerland, the Netherlands, Japan, and Germany. Following in the footsteps of these countries is an alluring prospect because they have been able to reduce waste, ensure universal coverage, have quite low wait times, and improve outcomes while keeping a private insurance system at the center of their system. This is remarkably helpful in the American context because it offers a method of healthcare reform that is compatible with Americans’ desire for choice and also because it keeps healthcare spending nominally private.

Systems which keep spending at least in appearance private may be more capable of increasing health expenditures at the rate required to accommodate the demand for new innovative but more expensive medical interventions and avoid excessive care rationing. There is a reason why Canada has the longest wait times in the OECD and Switzerland has the shortest. It appears that the political pressure to overly control costs is far smaller when the costs come in the form of premiums hikes (that can be blamed on insurers) and not new or higher taxes.

The retention of substantial private spending not only reduces the risk of excessive spending controls once a health policy is passed but also significantly increases the chance of successfully passing healthcare reform in the first place. The ACA learned the lesson of previous failed attempts at healthcare reform; single-payer is a tough pitch. Not only do you have to fight much of the medical industry, but also you have to increase taxes enough to grow the federal budget by somewhere between 50 and 100%. While these taxes would eliminate premiums, leaving many families NET better off, it is simply too big a political lift to be considered genuinely feasible for the foreseeable future.

Furthermore, retaining private insurance allows folks who desire to get more than the government-outlined basic standard of care to maintain freedom of choice. It also provides needed demand for newer, more expensive treatments and drugs that the government wouldn’t cover, thereby aiding medical innovation. In addition, private insurance can add value to the system by integrating with provider networks, such as is already done by Ascension Health, Kaiser Permanente, and many others. Such integrations may create better incentive structures and care management than could be reasonably expected from an exclusively publicly controlled model.

3. Managing the Competition.

Managed Competition uses a wide array of government interventions to make private insurance markets work better.

Insurers want to charge people with preexisting conditions more?

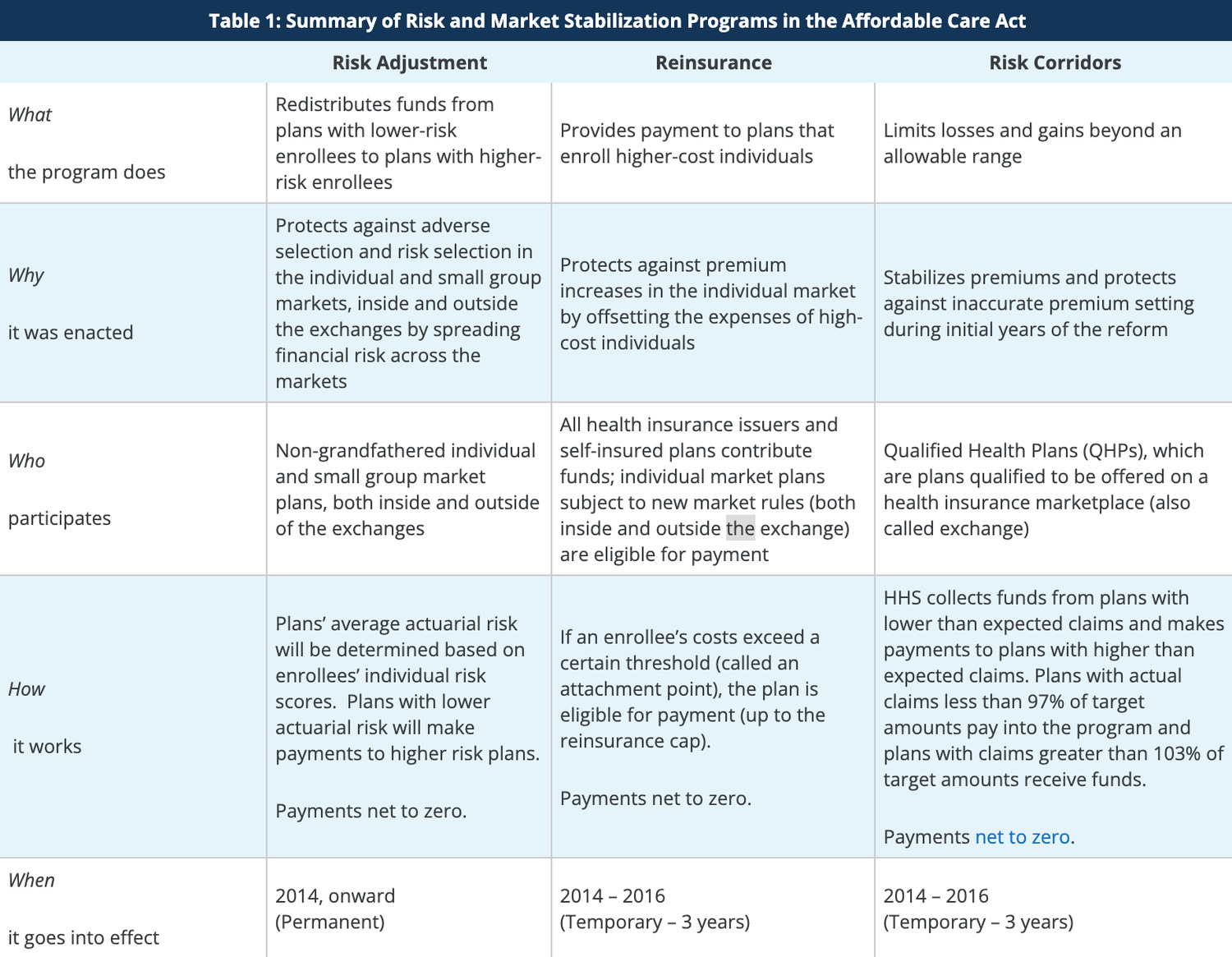

Require by law they don't price discriminate and correct on the back end by subsidizing insurers with riskier than average policyholders and charging insurers with less risky than average policyholders. (Glossary Terms: Community Rating, Adverse Selection, Risk Adjustment, Reinsurance, and Risk Corridors)

Consumers find it really difficult to make informed decisions between different plans?

Standardize deductibles and require all plans to cover primary care, emergency care, dental, vision, etc, so consumers can make an accurate apples-to-apples comparison. Further, create a centralized marketplace that makes competing insurance plans easier to analyze and compare.

Providers and insurance companies are incapable of negotiating consistent and reasonable prices for medical services and drugs?

Require providers to charge all payers the same price for the same services and drugs.

The model combines these exceedingly beneficial modifications to the private insurance system with a universal requirement that all individuals purchase insurance and an income-based subsidy that ensures everyone can afford it. In the end, you get a universal healthcare system that works just fine, although single-payer advocates will complain it's unnecessarily complex.

4. The Manager went Home Early.

The biggest problem with the ACA is that forgets to include certain essential features of the model, and other parts it only half articulates.

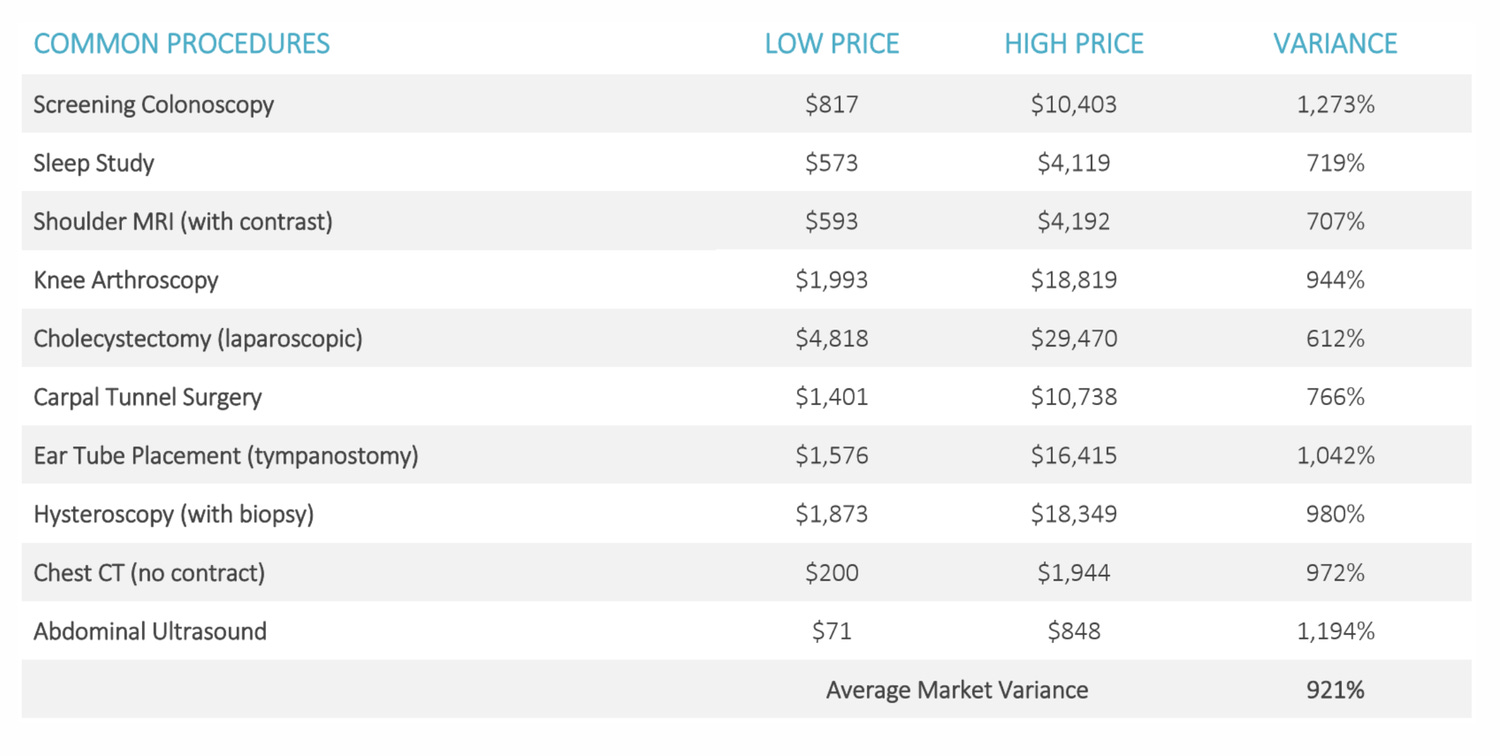

One of the most problematic omissions by far is the lack of All-Payer Rate Setting for providers. Currently, insurers pay wildly different prices for services. In one instance, the New York Times found that at a hospital in Boston, a knee MRI could cost anywhere between $830 and $4000 dollars, and this is not a particularly irregular occurrence.

Currently, Insurers and providers have to devote a lot of resources to haggling over prices. This, and the difference in reimbursement rates, is one of the contributors to America’s uniquely high administrative costs. This complexity also makes networks narrower than they would be otherwise.

Luckily, solving this problem is easy! All the government must do is require that providers charge one price to all insurers. If the government wants to aid in this process, it can organize central bargaining at the state level, but such a step is unnecessary for the reform to work.

Another problem is the inadequate level of standardization on the insurance marketplaces; in order for managed competition to work, insurance plans need to have the areas in which the differences only yield unnecessary intricacy standardized. Such is not so on the current state-based insurance exchanges the ACA created.

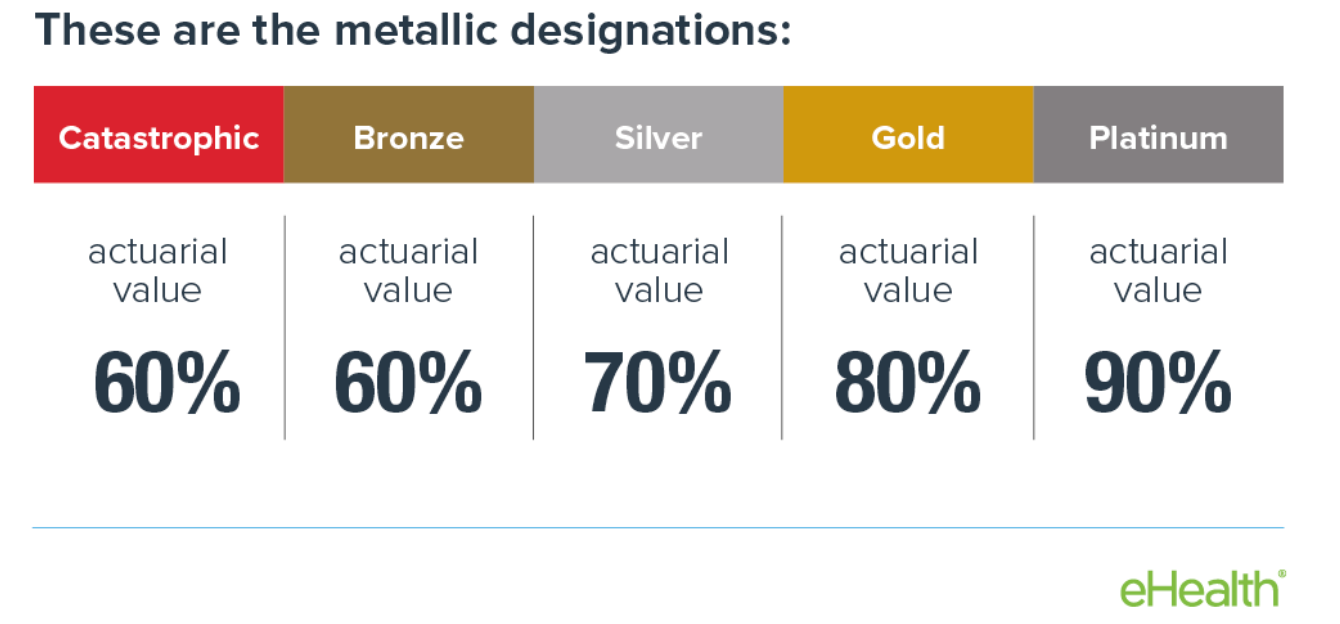

The current narrow standard package of benefits should be expanded, and the tier system, which introduces the unnecessary and unhelpful variable of the level of cost sharing, should be eliminated. The reality is that people who are opting for the catastrophic or bronze plans can face deductibles even as high as 8,000 dollars. That’s simply not an adequate level of insurance to guarantee their financial security. Meanwhile, people in Platinum plans face so little cost-sharing that they have little incentive not to overutilize care.

Tiers not only introduce the opportunity for people to underinsure or over-insure themselves, but they also make the task of risk adjustment far more difficult and worsen the risk that consumers act irrationally. Due to the immense number of variables that differentiate the different health plans on the exchanges, many select for a singular variable and base their decision almost exclusively on it. Most commonly, this occurs when people look for the lowest premium possible or the lowest deductible.

By removing this variable and standardizing deductibles and cost-sharing more broadly (either silver or gold), we embolden insurers to compete on what matters: monthly cost, speed/quality of care, and breadth of treatments and drugs covered.

Another issue is current risk adjustment procedures are imperfect, putting some insurers at an unfair advantage. It is difficult for the government to properly assess and rebalance risk pools. This can be fixed by encouraging states to launch and expand reinsurance programs. Reinsurance works by putting a lid on the amount of money an insurer has to spend on any singular patient. This is especially helpful to smaller insurers, where getting a few very expensive patients can make them go under quickly.

5. Where did everyone go?

Sometimes, we create our own boogeymen; in the case of the ACA, this boogeyman is the employer mandate it established. Through a shortsighted attempt to get more people insured, the ACA sabotaged its own marketplace by mandating businesses with over 50 employees purchase insurance but not requiring them to buy this insurance on the exchanges.

This was a bad decision; allowing businesses to bypass the exchanges leads to exchange plans having to charge higher premiums. It also leaves intact many of the normal problems of private insurance for a big section of the insured.

Employees are the victims; they get deprived of wages to pay for health plans that they get no say in, and then they lose their insurance (lest they deal with the pain that is COBRA) upon leaving their current employer. It’s a needlessly problematic system, and there are two possible solutions.

Solution #1 Universalize Health Reimbursement Arrangements

Instead of employers buying insurance on their employees' behalf, they will fund their employees’ purchase of private insurance on the individual marketplace.

Solution #2 End the Employer Mandate and Subsidy

Alternatively, we could just stop subsidizing employer’s purchase of group insurance and stop trying to force them to do so. Both these policies entrench the harmful employer-based system, and many of them avoid it anyway, using pesky legal tricks (like classifying their employees as contractors) to avoid having to do so.

Ending the employer mandate and the deduction that subsidizes their purchase of insurance will massively strengthen the exchanges and improve the well-being and mobility of the labor force.

6. A Public Option.

A key contributor to the fractured state of our healthcare system is the labyrinth of public programs that exist. We have Medicare for the old, state Medicaid plans for the poor, the Child Health Insurance plan for children, the VHA for veterans, and an endless number of other state and federal plans for public employees.

We also have credible reason to believe that private insurance is inferior to public insurance when it does not provide access to above-baseline level care or involve innovative payment systems, which leads to better provider incentives and reduced waste.

A public option represents the natural culmination of these two thoughts. It would allow us to roll many of the current people who rely on government insurance into one singular program, cutting down on the administrative waste we efficiency lovers despise so much. And it would do this while providing an opportunity to force private insurers to add value or perish.

What is crucial is ensuring that the Public Option is not given an unfair advantage over private insurers. It, like all other plans, should be listed on the exchanges and undergo the exact same risk rebalancing procedures that private insurers do.

If fans of public insurance are right, the plan will quickly become a very popular option and maybe even the de facto single-payer. If they are wrong, no one will be harmed in the process.

The final remaining feature of the public option is that it provides a convenient default plan to auto-enroll the uninsured into. Those who refuse to purchase health insurance will need to be forced to purchase it, and auto-enrollment with an auto deduction from their wages (for premiums) is the most direct way of ensuring this occurs.

7. Thou Shalt Have Money.

With Medicaid and CHIP gone, some may be wondering how payments for the poor will be organized. After all, in order to afford the public option or exchange plan’s premiums, some form of financial assistance is in order.

There are two elegant solutions to this problem. First, children should have their premiums zeroed out in full. If their parents have an exchange plan, this means the government will automatically pay for a special regulated child insurance plan from the same company. If the parent is enrolled in Medicare, the kid will be done so as well, free of charge. If the baseline level of care made available at the government reimbursement is less than desired, parents will be able to buy better plans at a very affordable cost.

Children are the least expensive of any age group in terms of healthcare; socializing their cost will not be too big of a burden and will yield huge benefits. Childhood poverty presently costs over a trillion dollars a year, and giving kids insurance paid for by the wallet of Uncle Sam will surely help ameliorate that problem. Furthermore, ensuring children's access to the health system can lead to life-changing care in the most crucial stages of development.

Second, in terms of those with low incomes, providing them subsidies exclusively through the public option is unnecessarily restrictive. Low-income people, like anyone else, should be given a choice to choose between the plans available to them, and a cash transfer deposited in a health savings account is an easy way of doing so.

For exclusively political reasons, we may want to means test this cash transfer since it will be comparably far more expensive than free coverage for kids, but in a perfect world, it would be universal.

8. We are a Federation, After All.

To many, the state-led model of the ACA has been a central weakness. Relying on states to expand Medicaid (which many refused to do) was a mistake, and even after all these years, Republican lawmakers have done their best to pretend their state’s exchange doesn’t exist. But this peculiar ideologically motivated indifference to the ongoings of their own healthcare affairs can only persist for so long and will be made impossible once employer-based insurance has also been rolled into the exchanges.

California, Maryland, and Massachusetts highlight the benefits of giving states the option to take the lead. In fact, many of the modifications to the ACA exchanges this article has proposed have already been done in the golden state, including the expansion of the basic package and reinsurance. Maryland, too, has some achievements to be proud of; it is the only state to currently use All-Payer Rate setting in its hospitals, with impressive results.

With this in mind, there would be no harm in the Federal government providing states the option to assume the custodianship of their public options and exchanges.

In the worst case scenario, Republican states will simply refuse the opportunity; in the best, some Democratic states accept the responsibility and leverage their less gridlocked political environment to make further reform.

9. Here is your bill, Sir.

While determining what institutions pay and what prices they pay is important, what’s also important is how they pay.

Presently, most care is compensated on a fee-for-service basis. Doctors get more money the more services they provide, creating an adverse incentive to over-test and over-treat.

The solution to this might be bundled payment (also called capitation). Instead of paying providers per service, we pay them a single price per the condition they are dealing with. This eliminates the negative incentive to wrack up the bill and puts the risk of avoidable complications from mistreatment on their shoulders.

But this is not the only use for capitated payment; with some integrated health systems and community health centers, a higher level of capitation has occurred. Rather than pay per condition, insurers pay one risk-adjusted price to the provider for caring for the enrolled person’s comprehensive needs.

This could encourage providers to maximize the integration and efficiency of their care and invest heavily in preventative interventions to reduce expensive ER visits and more intrusive interventions.

There are other payment system ideas that are worth consideration as well. Such as internal reference pricing as employed by the existing insurer, Side Care Healthcare.

10. Some Deregulation, as a Treat.

Wouldn’t it be great if we could have more doctors and inpatient/outpatient care? Well, luckily, axing some problematic regulations on the books could get us just that.

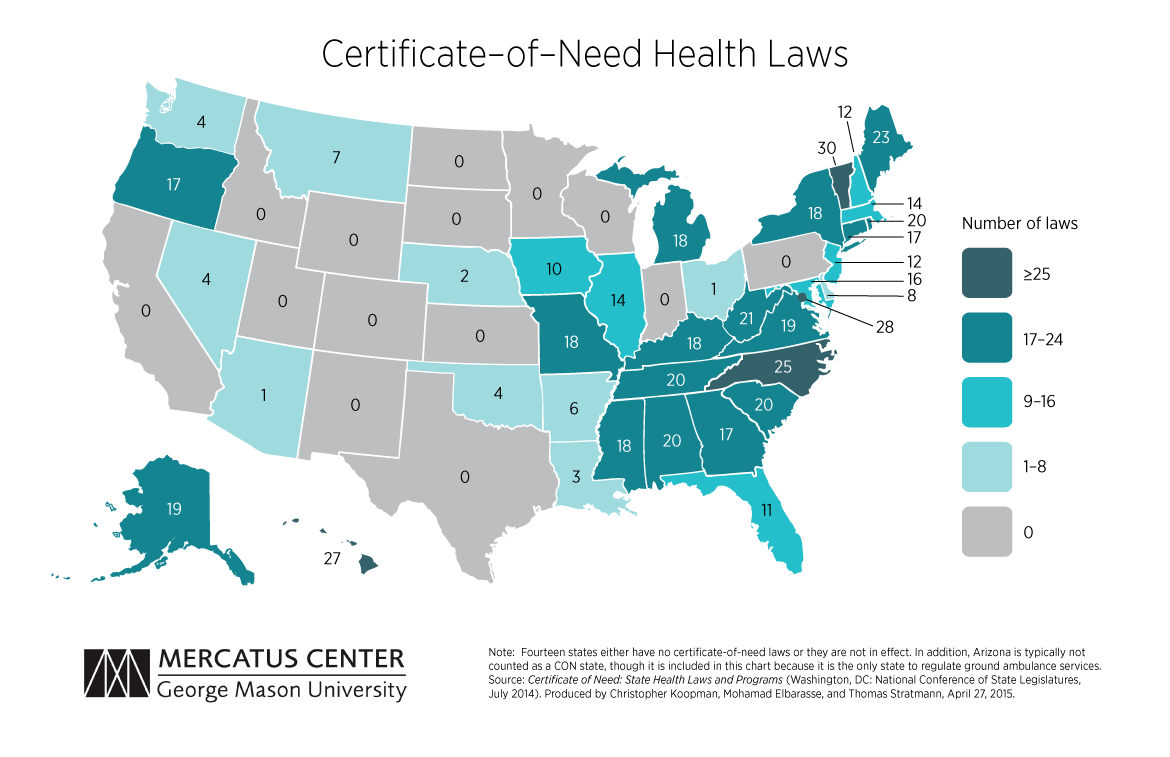

Certificate of need laws are a good start. Through some cognitive malfunction, policymakers in many states have managed to convince themselves that requiring explicit approval for doctors to expand their practice or for new medical enterprises to open up would help constrain costs.

This has never been the case. Certificate of need laws reduce access, degrade quality, and increase prices. The sooner they are scrapped, the better.

An additional issue is how difficult it is to become a doctor. Unlike some other countries, which allow students to go the medical school right out of high school, we require doctors to get a bachelor’s first. Acceptance to Medical School is also excessively challenging, in large part because of deliberate efforts by the American Medical Association (a doctor advocacy group) to constrain their supply and thus increase wages for present doctors.

We should copy what we have seen work in other countries. Let students go directly to medical school as they do in the UK, expand the number of seats at medical schools, and eliminate the renewal requirement for licenses, as Japan has done.

Everyone wanted the Affordable Care Act to work, and while it did secure some major gains in key areas, it never was going to suffice alone. Building a healthcare system that has universal access, better outcomes, and greatly improved efficiency requires fully implementing the model the reform was initially inspired by. This entails expanding and strengthening the exchanges, shifting from employer-level to individual-level insurance, adding in a public option, and opening up pathways for greater state involvement whenever possible. Supplementary systemic improvements can be achieved through the revision of payment systems and the elimination of harmful barriers to affordable care. Once these things are done, America can finally fulfill the promises of Obamacare and venture into a future with a population happier, healthier, and more financially secure than ever before.

Brilliant article that is clear and illuminating. I would vote for you to run healthcare policy if such a thing were possible

Left out of this discussion is the litigiousness of American culture. I know from experience that 1) doctors and hospitals tend to over treat and over-test, fearing that if they do not perform every test known to man, that should they err, it will come up against them in court. Likely it wont even get to that point, as the cost of defending a case alone would force the E/O insurance to settle out.

I also suspect that the frequency of liability lawsuits is playing a significant role. Right now, the insurance market is collapsing in Florida...why? One of the big drivers is the frequency of liability lawsuits. Florida is the worst, but certainly not the only state, where there is an incredibly perverse incentive for people to file lawsuits and claim injury. It works like this:

1) A small grocery store has a $1M million liability policy that they purchased for $1400 a year. Person slips and falls on a banana peel, they blame the grocery store, even if they dropped the banana themselves (I am serious here).

2) Person gets a lawyer who sends them to wink wink nod nod doctors. Doctor does an MRI of Person's back, revealing common degenerative imperfections like disc bulges/herniations. Doctor writes in their notes that, to their knowledge, this was caused by the fall and refers Person for spinal surgery.

3) Spinal surgery is performed, all billed under a Letter of Protection, an agreement where no one owes anything, but payment is contingent on the outcome of the lawsuit. To ensure the doctor/surgeon get paid and to give the case “shock value” for the grocery’s insurer and a jury, they pad the bills 5-10 times. $40k of treatment now becomes $400k.

4) Now the insurer has a choice. They can spend $120k defending the case, going to trial, and possibly losing, or they can settle for $500k now. They choose to settle almost every time. Why?

5) Say they choose not to settle, but fight it in court. They are not liable, right? After all Person droped their own banana! The grocery did nothing wrong. Imagine that the case goes to trial and Person wins. The jury is won over by the $400k in "medical bills" that the plaintiff owes and the “insurance company can afford it! (but remember they don't actually owe anything). The jury awards Person $2 million, including pain and suffering.

6) Now the insurer, which only insures the property for $1 million, has to pay the $1 million. But because of the way the law works, the court will look at the prior offer to settle at $500k and say “well you had a chance to settle, why didn’t you? Now you pay the whole thing” In the end, the court will remove the cap of insurance. That, or they risk getting sued by their insured for bad faith and paying treble damages.

Fact is, it doesn’t matter if the business owner is responsible or not. It does not matter if there actually was an injury or what the bills actually were. The insurer is left paying out huge sums of money so long as the billing is heavily inflated, and they are, every time. This is a strong incentive for people to get “injured” AND for the billing to be inflated. Not everyone is doing this, of course, but these outliers could be having a disproportionate effect on the cost of E/O insurance and the perceived health of Americans, and the cost of care.

Here, the “cost” of care is literally driving the claimed health issues, not the other way around.