A Land Value Tax For Houston

A better city is just a on good decision away...

Houston, we have a problem, the tax system being utilized by Harris County, Houston Independent School District, and the city of Houston is unnecessarily regressive and inefficient. As we speak, financial land speculators and big real estate owners are making bank, while our social services don't get the funding they need, and the poor suffer the burden of the sales tax. The residents of our city deserve better. Luckily enough, there is a tried-and-true alternative that can help us bring this about. The following short piece will discuss why switching to a land value tax as the primary source of revenue for our local governments would make Houston far more productive, prosperous, equitable, and egalitarian! Additionally, what specific policy features and strategies ought to be employed in order to make said proposal a reality?

I. STATUS QUO

To understand the problems with the current tax code, let's briefly analyze the sources of revenue for the three different local governments Houstonians live under.

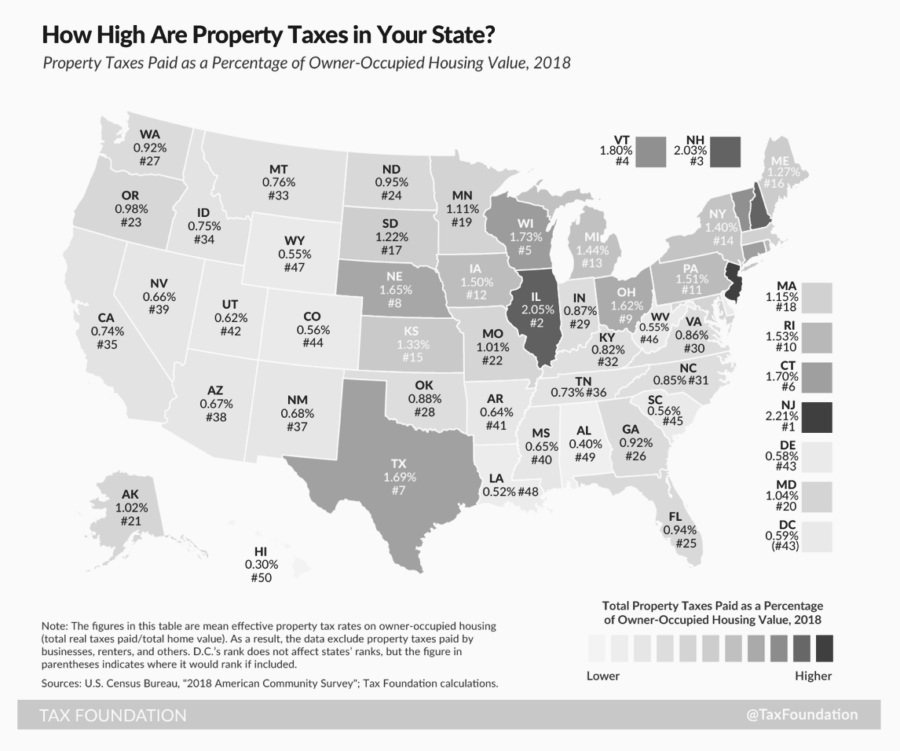

PROPERTY TAX: Far and away, the biggest source of revenue for all three of our local governments is the tax levied on properties. Currently, in Houston, each different level of local government applies their own rate on property, combining together to create, on average, an annual rate of 2.03% on the assessed value of a property. Property Taxes have a couple of major problems. First, they disincentivize development. When a developer takes a piece of undeveloped or underdeveloped property and makes improvements to it, they face a steeper tax burden because the value of their property went up. This punishes an activity that should be encouraged. Additionally, property taxes reduce business competitiveness. Creating a passive cost to owning real estate in the city means that some businesses that would otherwise like to come to the city will choose other locations to engage in their economic activity.

SALES TAX: Second place in local revenue raisers is the sales tax. While not nearly as large as the property tax, the City of Houston and Harris County do apply an additional 1.00% each to the state sales tax, creating a combined rate of 8.25%. Sales taxation of the local variant currently being used are highly regressive, create price distortions, disadvantage small businesses which rely on more business-to-business transactions than their larger competitors, and struggles with implementation/avoidance problems. A Value Added Tax, a tax, which also targets consumption, can be designed in such a way so as to not have these issues, but unfortunately, it cannot be administered effectively at a local level.

OTHER: In excess of these two taxes, revenue is also raised from various user fees on social services, revenue sharing agreements with the federal and state governments, fines, licensing fees, and a number of other sources. These additional sources of revenue are many and are generally justifiable. Although in certain areas, some modifications would be helpful, such as a transition from flat fine to progressive fines and creating new funding sources such as via congestion pricing for certain streets during high traffic periods.

For our purposes, we will focus our attention on simply replacing the Property tax, Sales tax, and whatever additional revenue is possible after that.

II. ALTERNATIVE

Land Value Taxation is exactly what it sounds like: taxation applied to the value of land. This means that, unlike property taxes, Land Value Taxes do not apply to any of the value added by the utility hookups, buildings, and pavements added. The idea was first envisaged by Henry George, an intellectual giant and political hero who spearheaded a movement for its implementation in the late 19th century. Over the years, George's ideas have been endorsed many times by thinkers, movements, and organizations scattered all over the map and the ideological spectrum. From Milton Friedman to Krugman to Stiglitz, to this day, land value taxation is one of the few examples of a major consensus among the right, center, and left of economics. The argument for it relies on the following line of logic…

No person is responsible for nor can increase/decrease the supply of land. Land is but a gift from nature; its supply is fixed, and its origin is non-human.

Land, being the essential factor of production it is, grows in value as the economy grows. When a landowner benefits from a rise in their land value, they do not do so because of any social contribution they have provided. Rather they merely appropriate the benefits by monopolizing something they had no role in creating.

No person is responsible for nor can increase/dee the supply of land. Land is but a gift from nature; its supply is fixed, and its origin is non-human.

Land, being the essential factor of production it is, grows in value as the economy grows. When a landowner benefits from a rise in their land value, they do not do so because of any social contribution they have provided. Rather they merely appropriate the benefits by monopolizing something they had no role in creating.

Since Land Owners do not naturally face any passive costs for monopolizing a parcel of property and are essentially guaranteed higher land values in the future, they are not adequately incentivized to fully utilize the land they own.

Given that no one produces land, a tax on land will not reduce the supply of land, which is something that cannot be said of taxes on property and investment.

Since the value of land is determined by supply and demand, taxing land will not simply lead to an overall increase in the cost of land. Rather, it will only work to appropriate some of the rental value of land for the public. For every percentage point of taxation on land, the value of land will drop until a point in which the amount of drop in land value will nullify any gains from raised rates. In this sense, a land value tax can be viewed as a land use fee paid to the public, based on the market value of land, and in such a way that permits some value capture on behalf of private actors if the rate is not raised to its revenue-maximizing point.

From the previous points, we can conclude that a Land Value Tax would easily raise a significant amount of revenue, be progressive since it only eats into the returns of private landlords/landowners, and increase the efficiency of land utilization and thus make housing cheaper, the economy more productive, and built environments denser.

III. IMPLEMENTATION

With a Land Value Tax, the city of Houston, Harris County, and Houston ISD could easily raise enough revenue to fund their current budgets and then some. But switching tax systems will require time if it is to go smoothly. Since the distribution of tax liability will be different under an LVT, with some paying more and some paying less, a period of shift is necessary. I suggest a simple four-year process.

FIRST YEAR: A two-rate property tax system is put in place, similar to those that already exist in dozens of localities around the United States. In this initial year, the tax rate on land improvements (buildings, pavements, piping, etc.) is cut by 33% and is offset by an increase in the land rate.

SECOND YEAR: The tax rate on land improvements is reduced by 50%, and the rate on land is increased to offset it.

THIRD YEAR: The entire tax burden on land improvements is eliminated, and the taxation on land values is set at a sufficient rate to raise the same amount of revenue.

FOURTH YEAR: Finally, the 1% municipal sales tax is eliminated, and its burden is transferred to land.

By the end of the four-year period, 100% of property tax and sales tax revenues will have been offset by LVT, and at this point, further raises to the rate on land will be possible and even advisable up unto the point where the rate has hit its revenue-maximizing threshold. Since there are so many areas where the multiplier on public spending is high, and LVT only eats into unearned private gains, there is no reason not to raise it to the revenue-maximizing rate.

IV. ANSWERS

Now, of course, there will be questions about the design of a land value tax. Here are answers to some of the most pressing ones for our proposal.

Would a sufficiently high LVT be legal under state law?

Currently, the state of Texas requires that local governments put up for referendums on any change to property taxes that would generate an increase in property tax revenue of 3.5% or larger. Whether this rule would apply to a Land Value Tax is questionable, but assuming it would, in the first three years of transition, this provision would not be an issue since the land value tax would only be raised to the rate necessary to offset the cuts to the taxation of land improvements. It is only in the final year that this limit will be exceeded. But at this point, a referendum would not be too much of an issue since voters would benefit from the counts and city sales taxes being eliminated in favor of a higher land value tax.

How would land values be determined?

There are plenty of good answers to this question. Digital Mapping tools like ARC-View, ARC-GIS, and GAMA have opened up the possibility of quick and precise land value assessment with no interaction with owners necessary. For those interested in learning more about these tools for tax purposes, I highly recommend reading this paper by Tom Nunlist. It should also be noted, that in the various places where LVT is currently being used, i.e. Singapore, Estonia, Taiwan, etc, plenty of valuation methods exist that Houston could use for inspiration.

For our purposes, I will briefly summarize what I believe to be the most precise approximation method in the case that these software programs or preexisting methods would not sufficiently do the trick. My proposed method contains two phases: (feel free to skip this section if you are not interested in in-depth explanations of highly advanced and complex tax evaluation methods)

SELF ASSESSMENT: A big dilemma that arises with all tax levies on illiquid assets is how they are valued. This is an issue faced by property taxes just as much as it is with land value taxes. See, in a market economy, prices generally reflect supply and demand. Suppliers want to sell their goods for the highest price possible, and consumers want to buy for the lowest price possible. With many consumer goods, prices are adjusted periodically in order to maximize profit. This is why when a commodity is in excess, it is put on sale, and when it is in shortage, its price is raised. But sometimes, the thing for sale is unique. Sometimes, there is no large institution that sets its price, and rather, its price is set right there and then by auction. In this case, it is often where the commodity goes to the person willing to pay the most for it, given that the price they are willing to pay exceeds the seller's minimum. Properties, like items up for auction, are necessarily unique. No two properties are the same. And thus, their prices reflect an active market process. This is where property assessment comes in. In order to demand a levy on land or property, the government must first know the value of the property in question. It is this valuation that determines the owner's liability at the end of the day. But since, as we mentioned earlier, the value of properties is not easily discernible due to each property's uniqueness, an issue arises. The people who are liable for the tax are incentivized to make their property seem like it is worth the least amount possible. Since property owners naturally know far more about their property than tax collectors, many times, assessments are produced that undervalue certain properties and then overvalue others in order to compensate.

One way this valuation dilemma can be rectified is through self-assessment with a private sealed bid auction. Under such a system, each year/or half-year (depending on design), each landowner will be required to submit their personal property valuation. At the same time, every property will be up for hidden backdoor bidding, where people who seek to buy the property submit privately the price they are willing to pay for it. In the case that a bid exceeds the value of the self-evaluation of a property owner, the owner will have two options. Either accept the valuation of the highest bidder and pay a higher percentage tax that year for under-assessing their property's value, or open up their property to inspection to the highest bidder with the risk that they may decide to purchase it, with the property owner legally required to comply. In the case the highest bidder opts out and decides the value they submitted was higher than the property is worth upon greater inspection, the property owner will be faced with the same two options with the second-highest bidder. Again either deciding to pay the tax plus fine or giving this bidder the opportunity to purchase their property for their submitted valuation. In the case, the property owner continues to choose to provide bidders the option to purchase, and all the bidders who submitted a value higher than the property owners back out, the property owner will only be liable for taxation based on their self-assessed property value. In the other case that one of these bidders decides their valuation was correct, the current owner will be forced to sell their property and pay the taxes based on the valuation of the bidder they sold to. To some, this mechanism may seem excessively complicated, but in fact, it really isn't. If property owners are reporting honest self-evaluations, they will usually not encounter a bidder who exceeds them. Even in the case they do, they should be enthused, not upset to see their property is worth more to someone else than it is to them because that means they can now sell it and receive more than cash than the amount the property is worth to them. Thus, this allows the government to save money on expensive tax assessors, increases the liquidity of the property market, and obtains the most precise property values possible. Another concern may be that few people will decide to bid on properties. If true, it may make sense for property owners to provide an artificially low value for their property. Thankfully, this is unlikely to be the case. After this tax evaluation measure is put in place, we can expect a new form of financial firm to emerge quickly that places bids on properties to capitalize on under evaluations.

LAND VALUE ISOLATION: The aforementioned process showcases how the most precise value of properties can be isolated, but it does not determine for us the actual land share of a property's value. Land is just one component of a property's value, along with the improvements that have been made to it. To isolate the land share, various algorithms have already been designed and tested. These algorithms, when provided with the information about a property, such as the square footage, the number of bedrooms, bathrooms, etc., can use this information to determine what percentage of the property's value is land. Considering that said information is readily available on applications like Zillow, creating an automated process for finding the land value out of a provided property value is simply an exercise of plugging in data and letting an algorithm do the work. Some support using this comparative algorithm method to also find the property value, although I tend to be of the view that while this would not be terrible, it would also be not nearly as precise as the previously mentioned method.

How often would an LVT need to be paid?

It depends on the land value approximation method in use. In the case that digital mapping tools can get us there, then pretty frequently. Frequent payments stabilize government revenues and reduce payer liquidity risk. But given that such a method was, for some reason, not usable, an annual/biannual schedule would be necessary in order to not have excessively high administrative costs.

Now that we have established the whys, whats, and hows of transitioning from Sales and Property Taxes to a Land Value Tax in Houston, a question remains, "ok, now what?" As I have demonstrated, an LVT would benefit most people, especially those in the working class, certain parts of the middle class, future generations, and pretty much everyone who does not own a lot of valuable land in Houston. But the minority it will leave worse off is, unfortunately, an extremely powerful one in local politics. With these folks being local landowners with low to mid-density improvements on their land. The same group who is also responsible for other bad policies in our city, such as setback and density limits, parking minimums, and draconian private deed restrictions

Confrontation with this oligarchic minority is necessary to make any progress in our city, but it will not be easy. The key to our success will be marketing a transition to an LVT, not as a new onerous tax to worry about but rather as the elimination of taxation on real estate and sales in a way that will leave most people far better off!